EP93: Glazed Over

Stock Ideas From Investment Professionals

Welcome, subscribers!

This week, we’re happy to share a highly eclectic batch of stock pitches.

If you enjoy what we do, please consider forwarding to a friend or colleague who might also appreciate our work.

Keep reading as we share 5 new ideas, including:

An iconic consumer brand changing its go-to-market strategy by expanding partnerships with major retailers and restaurants

An automotive and industrial parts distributor with a robust brand and strong network, positioned to capture market share in a fragmented industry

A unique bank serving a specialized (and highly profitable) niche

An online platform connecting buyers and sellers of customized manufacturing products

Keep reading to learn more.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

As an addendum to their most recent investor letter, White Brook Capital released a detailed write-up on their newest position in Krispy Kreme (DNUT). Krispy Kreme, the iconic donut brand, is transforming its go-to-market strategy by prioritizing partnerships with major retailers & restaurants rather than relying solely on its own storefronts. White Brook sees upside in excess of 30% in the near-term.

Krispy Kreme Inc (DNUT)

Valuation

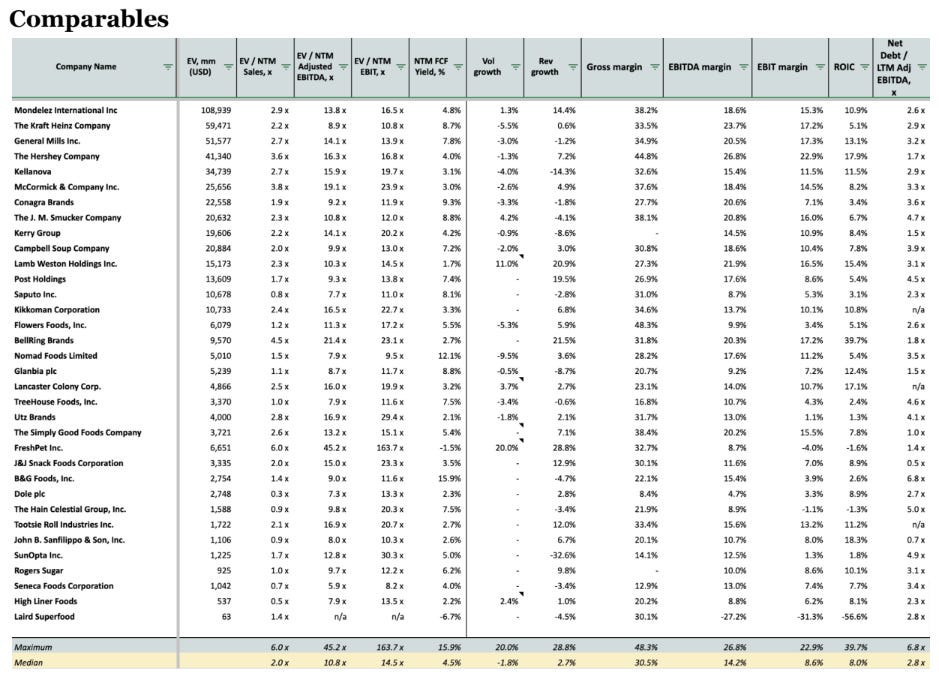

Relative to its CPG comparables (last page), Krispy Kreme is cheap on sales and EBITDA given its growth prospects and gross margins that post investment cycle will result in significant and underappreciated free cash flow generation. While the Company is currently spending to enact its growth strategy, by mid 2025, its long-term economics should be apparent and reflect 20%+ EBIT margins, and improving free cash flow conversion on top of strong growth both in the United States and internationally. White Brook believes consensus estimates, starting in 2025, but certainly in 2026 are low, and that the company is more profitable and will generate returns on invested capital at least better than average for the industry. We believe the stock can rerate to $15 by mid 2025 in a base case as investment intensity declines, and significantly better than that should its partnership with McDonalds prove out.

Company Description

Krispy Kreme domestically owns, and internationally franchises and owns retail donut stores of the same name.

The Company has bought in its franchises in a majority of its regions. In 40 countries it operates and serves donuts in its own retail locations and distributes boxes and single serve donuts to third parties including grocery stores, retail stores, and most recently quick service restaurants.

Dunkin Donuts and Krispy Kreme account for ~55% of all donut shops in the United States. Krispy Kreme legacy retail locations are predominantly “hot light theaters” that house their proprietary donut making equipment that can make up to 12,000 donuts a day. The Company’s stores typically produce donuts two times a day, and when donuts are actively coming off the line, a red “hot light” is turned on outside (and in their app) indicates that in-store the donuts are fresh and warm. It’s a superior donut experience and one that has built significant brand equity.

It also distributes boxes of donuts and single serve donuts from these stores to other retail and grocery stores including Walmart, Target, Kroger, Safeway, Giant, Publix, etc (“doors”/”spokes”), but they are not yet in all of those retailers' locations. Unlike during the early 2000s, the Company now owns a majority of its stores and markets. In the early 2000s stores were frequently franchised and donuts delivered to retail stores were sometimes/often leftover retail donuts with franchise owners hoping to monetize their waste. Today, the company “Delivers, fresh, daily.” Delivering fresh daily, and collecting the waste from the previous day is a superior experience for their customer (the retailer), the consumer, and for Krispy Kreme’s data collection and brand equity. In the 4th quarter the Company moved from a pilot with ~100 McDonald’s stores to the beginning of a roll out to 12,000 McDonald's locations over the next two years. On the third quarter earnings call, it accelerated the number of stores Krispy Kreme would be served in from 1,000 to 2,000.

The Company’s IP includes its differentiating donut recipes; It’s differentiating donut making equipment; and its national footprint which makes it an attractive partner for national brands like Dr. Pepper, Kit Kat, and the NFL on the “content” side, and large retail and grocery chains on the “distribution” side.

For the uninitiated, Krispy Kreme donuts are noted for their light and fluffy texture and well applied glaze that gives the donut a sleek, cared for, appearance that “melts in your mouth”. A cold Krispy Kreme donut is good, but the donut is best consumed warm, at a retail store, or a 10 second stay in a microwave. It’s hard to have just one.

The Company also operates internationally. Large international market hot light theaters outperform US locations by ~2x and do approximately $10 million USD in average transaction volume. The Company’s operates a similar “hub and spoke” strategy in both. The Company owns international region operations outright, through JVs, and via franchises with smaller countries more often franchised. On the 3Q24 earnings call the company indicated it was leaning into the international Franchise opportunity which appear to be both a reflection of the remoteness of some of the newest operations, and the light capital intensity given current needs in the United States. It’s important to note that unlike chocolate, most cultures have a flour and concentrated sugar treat culture and the concept travels extremely well.

JAB Holdings is the largest shareholder of the Company. JAB is anchored by the Reich family, but in their private equity funds, they also have minority limited partners. Krispy Kreme was bought by one of JABs private equity funds in 2016, and in the IPO in 2021, stock was distributed to minority partners, even while the family increased its stake.

Recent History

Krispy Kreme’s stock evokes bad memories for many.

Previous to the buyout by JAB in 2016, the Company operated a franchise model. The Company expanded too quickly with a management team that allegedly played fast and loose with their accounting treatments creating an opportunity for JAB Holdings to buy Krispy Kreme in their private equity fund along with several other fast casual and breakfast concepts, like Keurig and Panera Bread.

JAB made significant strategic changes after buying the company.. The firm turned over the management team and supported a strategy shift from franchises and a bad consumer products effort to owning operations and ultimately exiting the consumer products business. Owning operations improved operational flexibility, setting up the current hub and spoke distribution model.

JAB took advantage of an ebullient market for IPOs in 2021 to distribute half the firm’s position in Krispy Kreme to its minority LPs who largely monetized indiscriminately, driving the price down to the low double digits (even while the family added to its position). While the Company was able to grow post-Covid and had a story to tell, it was still early in the shift to the current operating model and free cash flow generation was negative - a hard story for long-term value investors to buy. While it was never a Wall Street Bets favorite, it has been frequented by and commented upon by retail investors who recognize the donut's superior quality. Many were caught in IPO shareholder indiscriminate selling of 2021 and 2022. Many early public shareholders have been burned.

Today, wall street analysts often compare the Company to franchised restaurant stocks. It’s a bad comparison. Average QSR volumes are between $1-4mm vs Krispy Kreme’s $5mm. QSRs predominantly sell to consumers, while Krispy Kreme’s business is increasingly moving to a B2B2C model where stores distribute to retailers who sell to consumers. Furthermore, good restaurant stories are able to turn tables more quickly (or at least walk in throughput), lower cost, raise prices, add new menu items, and improve the takeout business to improve their unit economics. Krispy Kreme will improve economics by driving more specialized donut sales, increasing their distribution points, efficiently delivering to those points, and reducing waste. They are closer to a CPG than a restaurant and therefore a poor fit for industry specific analysts. Their EBITDA and FCF growth will differentiate and force uninterested investors to take notice.

BENCH Evaluation

White Brook’s BENCH analysis determines whether the company has a competitive advantage by evaluating whether the product is the Best, Easiest, Necessary, or Cheapest in their category and whether the management team is compensated appropriately for its success (Heart).

White Brook requires that a company’s product or service has two qualities and is developing a third to be on its “bench” of portfolio companies.

BEC: Krispy Kreme donuts themselves are the best mass-produced donuts particularly as it compares to Dunkin or a par-baked/air-fried grocery store donut - its direct nationwide competitors. In early October, Mondelez announced a minority investment in a lower calorie, baked donut that isn’t meaningfully distinguishable from a grocery store donut. From YouTube video reviews, it appears to be a diet donut:

“It’s not bad, it doesn’t have the texture of a Krispy Kreme donut. Krispy Kreme has that nice [bite and thinking]…mmm it’s not bad…cannot say it’s great. But I guess if you’re dieting because this has half the calories of standard Krispy Kreme donuts..”

While US northeasterners have a provincial preference for Dunkin, that preference fades as exposure to Krispy Kreme increases.

The Company’s implementation of a hub and spoke strategy makes Krispy Kreme donuts readily available without the same capital intensity of establishing retail-only stores or kiosks nationwide. As the product rolls out to McDonalds over the next two years, they should become even more accessible than Dunkin Donuts.

A grocery store has limited opportunities for differentiation. For many, the bakery is to the grocery store what “live sports” are to television - it draws attendance and differentiates. Within the bakery, there are multiple offerings, breads, bagels, cakes, and donuts. Breads and cakes can demand a premium, and given the overall price, a meaningful profit can be earned on each of those SKUs. Donuts are typically provided to fill out the bakery’s assortment. Most grocery stores “complete” their bakery offering by selling par-baked/par-fried donuts that just need to be finished by baking in their standard oven and glazed, resulting in a doable, but relatively poor experience that they then charge ~$1 per donut for.

White Brook estimates that for a half dozen donuts, grocery stores make about $2.50 per box for their par-fried donuts while collecting a retail margin of about $1.80 from a Krispy Kreme box. Given the limited quantities of store-made donuts sold by grocery stores, even with limited demand uplift from providing a better donut, given the reduction in operational complexity by not making store donuts, selling Krispy Kreme donuts has a positive return. Additionally, with Target and Walmart beginning to stock Krispy Kreme donuts - as well as other grocery stores, it’s difficult for a grocery store to operate at a quality disadvantage to those mass market stores.

The Opportunity

2021 and 2022 were a story of a turning over investor base. 2023 married a still nascent strategy change with elevated leverage and negative free cash flow. 2024 suffered from the same plus a NLP1 weight loss drug threat that is proving less than formidable for Krispy Kreme in particular.

2025 should begin to see the fruits of the hub and spoke model ripen. While depressed margins will still be present in the first half of the year as the Company grows its store count and builds out its distribution network to fulfill and expand into the McDonald’s contract, the eventual FCF production should become obvious to numerate investors relatively quickly. If the roll out goes as expected, it’s also possible that despite themselves, there will be EBITDA and FCF upside and relatively tightly forecastable and significant growth for the next 3 years. In 2026 as critical mass in hubs is built nationwide and new QSR and retail chain doors become increasingly incremental, free cash flow should be significant.

What matters:

The Company’s international business is strong, represents 30% of revenue, has a solid margin profile and is growing quickly, and is worthy of its own analysis for long term holders. It isn’t the reason to buy the stock today.

The stock’s short to medium term performance depends on the roll out of the direct fresh daily strategy nationwide and in particular with McDonalds. By piggybacking/partnering with McDonald's - an organization that has studied and located some of the best food retail locations in the country, the Company has an anchor customer to build its hubs to match, nationwide. McDonald’s also has the required scale to provide an immediate return to Krispy Kreme, as well as a platform to make exceptional returns servicing other parts of the food ecosystem.

Much of the risk of the McDonald’s contract is mitigated by the long and expansionary pilot that the Company conducted with McDonald’s over the past year in Indiana and Kentucky. On the 3Q24 call the rollout was further de-risked as Krispy Kreme 2x’d the number of restaurants that they will service by the end of the year to 2,000. It’s likely that both McDonalds and Krispy Kreme had to agree to accelerate the timetable, and is an indication of McDonald’s satisfaction with early performance.

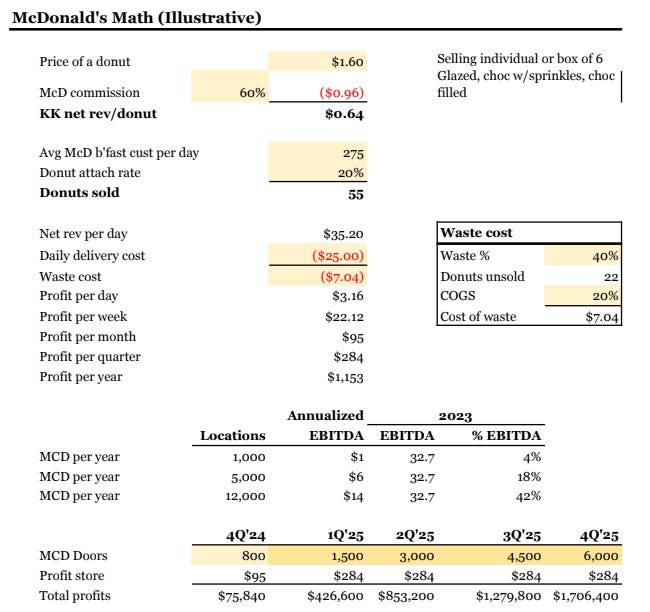

Krispy Kreme is rolling out to 12,000 (again will be ⅙ rather than 1/12 the way through by 2024 year end) McDonald's locations selling single donuts and half dozen boxes in their standard glazed, chocolate covered and strawberry covered SKUs. I’ve outlined the math below for a single donut, the last attractive for Krispy Kreme. It’s also worth noting that a single donut is amongst the cheapest items on a McDonald’s breakfast menu.

Early reviews of the experience appear to be overwhelmingly positive.

The real question is throughput. On the 3Q24 call, the Company pushed on answering a direct question about what the attach rate was, but the Company did indicate that donuts were occurring in all day-parts, not just breakfast. This aligns with the above reviews, but proves that my analysis below, while directionally correct, is a bear case and not a realistic base case.

It’s also important to note that the Company has the ability to mitigate underperformance and enhance returns by adding other QSRs to the platform. It is a non-exclusive partnership for Krispy Kreme.

White Brook is always focused on negative workflow streams, in this case the waste. As part of their deal with McDonalds, Krispy Kreme collects the waste daily upon delivery of the new fresh baked donuts allowing the Company to triangulate against receipts and ensure McDonalds, a franchisee, or a rogue employee isn’t five finger discounting its product. It also allows the company better understand local demand, and vary its deliveries accordingly.

On the 3Q’24 they further de-risked the effort by indicating that they have the ability to outsource delivery to McDonalds to delivery companies. This a big deal and allows Krispy Kreme to focus on making donuts, making new donuts, and marketing them worldwide.

On the call they also mentioned they now have an agreement to deliver to CostCo.

McDonalds Math

It’s important to note:

The effort is profitable at relatively low levels of throughput.

We also have no indication of McDonald’s commission, but believed 40% was a reasonable base case.

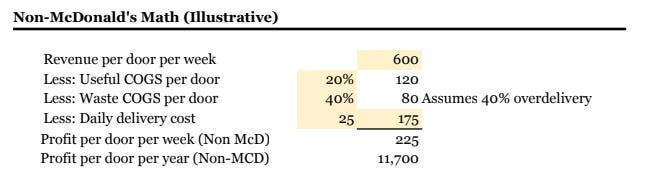

Krispy Kreme believes they can service 100 doors per hub fleetwide, more for newly constructed hubs that are purpose built for delivery. They are building 30 new incremental hubs to service the nationwide opportunity at fully employed spend of between 3-6mm, so 180mm of capital and operating expenditure over the next 2+ years. If each of those doors is a McDonalds, the returns outlined, are respectable unlevered returns. In reality however, there will also be non-McDonald's doors added with better economics - the Company expects 12,000 new McDs through 2026, and 3,000 non-McDonalds. Importantly the current average revenue per door per week for a non-QSR is ~$600, and therefore has much better profitability than outlined above.

The donuts per McD store in particular are probably significantly conservative, and the value add of the newly added non-McD stores is solid and likely to improve further from here. I find the returns in a base or upside case, extremely compelling and believe that the Company is on the verge of being able to both invest in its growth and harvest cash flow at the same time. While the Company has indicated that 3Q25 should begin to see sustainable year over year margin expansion again (and even some in the 4Q this year, given extra costs in 3Q24), we think the free cash flow the company begins to generate in the second half will also be impressive given its growth and a classic and quick deleveraging from paying down debt and quickly growing EBITDA will result in a rerating of the Company’s cash flows on cash flows beyond current expectations.

We share 4 more ideas below with our paid subscribers.

Note: If you’re still on the fence about subscribing, consider asking your employer to fund the purchase.

We’ve provided a potential script below!

Hi [manager’s name],

I’d love to expense my subscription to Elevator Pitches! It’s a newsletter full of the best stock pitches curated from the letters of professional investors. Here are two examples (here and here) of the types of posts they deliver each week. The paid subscription will give me access to every stock write-up they surface.

Because the newsletter is an educational resource, I was hoping that it’s something that can be expensed to [insert company name]. It is $90 for the whole year, which is a steal considering all the insights and learnings I will get from it.

Thank you so much for considering