EP92: Fair To Middle-ing

Stock Ideas From Investment Professionals

Welcome, subscribers!

Since our last edition, we’ve dug through another batch of investor letters, and we’re here to share only the best ideas.

If you enjoy what we do, please consider forwarding to a friend or colleague who might also appreciate our work.

This week, we have 7 new ideas to distribute, including:

A well-established industrial distributor, currently capitalizing on the surge in electric and tech infrastructure.

An IT outsourcing firm battered by a cyclical downturn, but primed for a resurgence as digital demand rebounds.

A new building products roll-up led by a seasoned executive, aiming to consolidate a fragmented industry with a bold growth strategy.

A recently offered buyout target in industrial services, blending diverse divisions in building products, energy, and specialty metals.

Keep reading to learn more.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

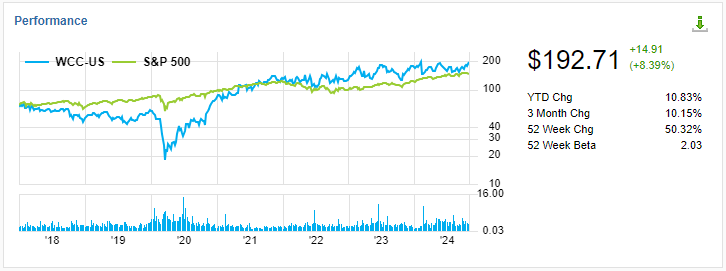

Blue Tower detailed their investment thesis for Wesco International (WCC), an industrial distributor. The shares jumped 8% today on a strong earnings report, but Blue Tower still sees plenty of upside in this durable grower.

In this letter, I will be exploring our holding in Wesco International, an electric infrastructure, component, and communication equipment distributor. These distributors are another indirect way to profit from the ongoing boom in solar technology, electric vehicles, and AI technology. Despite the big boost that these technology trends should provide to these distributor businesses, these distributors are not trading at the expensive multiples of AI-related stocks. While most electric component distributors are benefitting from these trends, Wesco is still realizing the integration benefits from a major 2020 merger and is more levered than peers.

Wesco Business Overview

Wesco originated in the Westinghouse Electric and Manufacturing Company in 1922, where it was originally the distribution arm of Westinghouse’s electrical and industrial products.

On February 1, 1994, private equity firm Clayton, Dubilier & Rice (CD&R) purchased Wesco from Westinghouse in a $340M leveraged buyout. Wesco was again sold just 4 years later to The Cypress Group which created the holding company Wesco International. In 1999, the company went public. Over the past 20 years, Wesco engaged in over a dozen acquisitions, growing the scale and geographic scope of the company. In 2020, Wesco completed its largest acquisition with the takeover of Anixter International when it used a combination of cash, Wesco shares, and preferred stock to beat out an offer from CD&R.

The company is headquartered in Pittsburgh, PA and is focused on supplying the US market and generating 85% of their business revenue coming from the USA and Canada. They are a business-to-business distributor and provide services related to logistics and supply chain management. Their business is organized into three operating segments: Electrical & Electronic Solutions (EES), Communications & Security Solutions (CSS) and Utility & Broadband Solutions (UBS).

Sales for the company have seasonality with reduced activity in Q4 and Q1 due to weather affecting customer projects. This kind of distribution business is attractive for several reasons.

The company has a fragmented suppliers (over 50,000 suppliers in 2023) and a fragmented customer base. These customers range from large Fortune 500 corporations to local small businesses. Acting as the distributor in a fragmented marketplace like this gives Wesco considerable pricing power as it limits the bargaining power of both their suppliers and customers against them. From their 2023 10-K:

“We have a large base of nearly 150,000 active customers across commercial and industrial businesses, contractors, government agencies, educational institutions, telecommunications providers, and utilities. Our top ten customers accounted for approximately 11% of our sales in 2023. No one customer accounted for more than 2% of our sales in 2023.”

Distributors have lower capex requirements compared to manufacturers and can turnover their inventory quickly. This fast turnover is important for adapting to changes in technology and industrial demands. Wesco’s asset turnover and inventory turnover ratios are roughly in line with other distributor businesses but declined from their pre-Covid averages. We believe this is likely due to the company carrying extra inventory to avoid any potential supply chain disruptions like what the industry experienced during Covid-19. Wesco announced a $500 million investment program to develop various digital projects. Initially, this will focus on upgrading their ecommerce platform, modernizing their supply chain, automating internal processes such as order fulfillment, and hiring tech talent. Their 2022 purchase of Rahi, a data center services company, also was part of this digital transformation strategy. Despite these investments the company is making in software and their digital sales channels, it normally has limited capex requirements. As a result, the company announced a target of achieving free cash flow of 100% of adjusted net income1.

Due to the recent supply chain disruptions starting in 2020, many corporations are resourcing parts of their supply chain from North America. This reshoring of the supply chain will act as a tailwind for distributors like Wesco.

Wesco is focused on forecasting the needs of their customer base and adjusts their inventory accordingly. As a result, their cash flow generation tends to be counter-cyclical in a recession as they will reduce inventory in the face of falling demand, thereby also reducing their working capital requirement.

The increasing scale of Wesco affords it economies of scale, operational leverage, and cross-selling opportunities. The business sector of industrial, electrical and utility distributors is still unconsolidated and as Wesco grows its competitive advantages grow with it. Due to their operational leverage, the company has guided that they believe EBITDA growth will be twice the rate of their sales growth.

Secular Growth

There are huge secular growth drivers for electrical equipment distribution. While many other companies exposed to these tailwinds are trading at lofty valuations, the distributors are still trading at relatively cheap valuations despite them standing to benefit even more than other businesses due to their inherent operational leverage. Electric vehicle adoption will lead to new opportunities in charging infrastructure and components. Solar energy is the fastest growing renewable energy source. Wesco is well suited for the rapid expansion of solar installations as it partners with leading solar manufacturers to offer photovoltaic modules, inverters, racking systems, and load balancing equipment. Data centers are still rapidly growing in number. A Goldman Sachs Research estimate projects data center power consumption will increase 160% from current levels by 20302. Wesco is poised to capitalize on the need for reliable power infrastructure and energy-efficient technologies. AI will serve as a further accelerant to this growth as AI workloads require significantly more energy than traditional computing tasks.

Management Guidance

Management has guided that they believe the company will be able to expand margins through operational leverage, gross margin expansion, digital transformation software projects, and further acquisitions. The current 2024 outlook for EBITDA margin is 7.0-7.3% but the company is guiding to a future target of 10%. Long-term sales growth rates will be 5-8% with 4-6% coming from organic growth and 1-2% from acquisitions. Their leverage target is 1.5x-2.5x net debt / EBITDA and they’ve rapidly moved towards this range since integrating Anixter.

Buybacks

While Wesco pays a small dividend, it is also deploying significant amounts of capital on buybacks and has accelerated these buybacks this year. In Q1 and Q2 2024, it purchased $350 million of stock, retiring over 4% of outstanding shares. This is part of the $1 billion share repurchase program the company announced on June 1st, 2022. The company intends to opportunistically repurchase stock and preferred shares depending on market conditions and the company’s financial resources.

Competitor Comparison

While Rexel headquartered in France is the most similar publicly traded company to Wesco, I included three other US-based distributor companies for comparison. Avnet and Arrow Electronics are more IT focused, but have some overlap with Wesco’s electronics business. W.W. Grainger is the largest industrial distributor in the USA.

Many of the tailwinds that Wesco are benefiting from also help their competitors, especially Rexel. If any of these companies become materially cheaper than Wesco, it may be wise to reallocate to them instead.

Rate Sensitivity

Roughly half of the debt of the company is in variable rate borrowings. Their fixed rate debt has maturities ranging from 2025 to 2032. According to the most recent 10-k: “A 100 basis point rise or decline in interest rates would result in an increase or decrease to interest expense of $25.2 million under our current capital structure.” Therefore, falling rates will have a significant benefit for the company.

Forward returns

For investment ideas predicated on a company compounding through predictable, steady growth, I believe it makes more sense to evaluate the companies as providing a forward rate of return rather than a specific price target. Wesco’s recent revenue growth has been largely from acquisitions and it is unlikely they can continue this growth going forward as can be seen in growth guidance from management. Using management’s guidance (their guidance appears reasonable), Wesco provides a forward rate of return of 17.5%, with 9.5% from its forward free cash flow yield (using the low end of FCF guidance) and 4% from its organic growth of revenues and 4% from the management’s guidance of margin expansion.

We share 6 more ideas below with our paid subscribers.

Note: If you’re still on the fence about subscribing, consider asking your employer to fund the purchase.

We’ve provided a potential script below!

Hi [manager’s name],

I’d love to expense my subscription to Elevator Pitches! It’s a newsletter full of the best stock pitches curated from the letters of professional investors. Here are two examples (here and here) of the types of posts they deliver each week. The paid subscription will give me access to every stock write-up they surface.

Because the newsletter is an educational resource, I was hoping that it’s something that can be expensed to [insert company name]. It is $90 for the whole year, which is a steal considering all the insights and learnings I will get from it.

Thank you so much for considering!