EP49: Cash For Clunkers

Stock Ideas From Investment Professionals

Welcome, subscribers! Today, we share pitches for 6 interesting ideas, including an automotive retailer, a video game engine platform, and a small cap cyber security company. Read on to learn more. 📕👇

We appreciate your support. If you enjoy this issue, please forward to a friend or colleague!

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

Silver Beech Capital provided an in-depth look at their thesis for Asbury Automotive Group (ABG), one of the largest automotive retailers in the United States with a playbook to roll up a fragmented industry. Silver Beech also included a brief pitch for another new holding, Playa Hotels & Resorts (PLYA), which is a company we also shared back in May.

Asbury Automotive Group (NYSE: “ABG”)

Asbury Automotive Group is a mid-capitalization company and one of the largest automotive retailers based in the United States. Asbury operates 190 franchises located primarily in southeastern and southwestern metropolitan markets. The retail automotive industry is highly fragmented, however Asbury has generated outstanding ~20% compounded returns for shareholders over the last ten years. We believe the factors that helped the company achieve this success remain in place today and that Asbury’s intrinsic value exceeds its June 30 share price by more than 40%.

Asbury’s success resulted from nearly doubling its franchise footprint in the past 10 years from 98 franchises to 190 franchises (152 dealerships / 38 collision centers). Asbury profitably doubled its footprint by acquiring and integrating franchises at attractive prices. To underline the scale of Asbury’s capital deployment: in 2012 the company had ~$1.4 billion of capital deployed, by 2022 this figure had grown 5x to ~$7.4 billion. Clearly, Asbury saw an attractive opportunity in franchise acquisitions.

Asbury has an operations playbook for its new acquisitions that (i) improve franchise operating efficiency (more inventory turns, floorplan financing, geographical clustering within a market for scales of economy); and (ii) sell higher margin and less cyclical lines of business (parts/services and finance/insurance products). Based on our studies of Asbury’s acquisitions and financial history, we estimate that Asbury’s after-tax incremental returns on capital were ~13%+. Asbury’s historically high debt levels helped turn ~13% incremental returns on capital into greater than 20% incremental returns on equity. Attractive capital deployment, high reinvestment rates, and leverage drove returns.

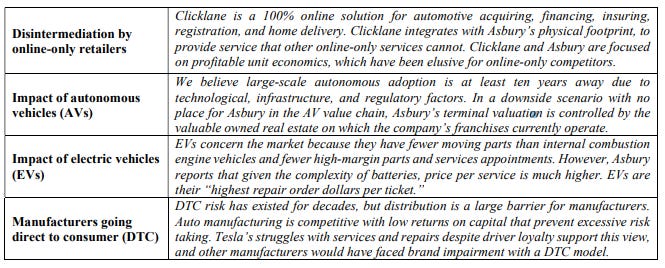

Asbury’s management team continues to outline a large pipeline of franchise acquisition opportunities that should reward shareholders. Further, we believe Asbury’s go-forward incremental returns on capital might even exceed past returns driven by two capital-light product additions to its operations playbook: (i) expansion of its finance/insurance business line into repair/maintenance contracts through a 2021 acquisition named Total Care Auto (TCA); and (ii) franchise integration with Clicklane, Asbury’s online vehicle retail platform.

Broadly, we believe public markets have undervalued automotive retail companies based on risk factors against which Asbury has thoughtfully prepared itself:

We believe Asbury is an attractive investment for the following reasons:

Less cyclical cash flows: Asbury employs a razor–blade model, with cars sold as the low margin “razor”, and finance/insurance and parts/services as the higher margin “blade”. The “blade” segments represent only 19% of revenues but 61% of gross profits, are not as cyclical as automotive sales, and are growing share of profit as new service capabilities are integrated.

Management track record of strong capital allocation: The large opportunity remains to acquire franchises at attractive 13%+ after-tax returns on capital. Asbury has a lower leverage level than management’s target range which provides capacity to deploy capital via franchise acquisitions and share repurchases. Management has opportunistically repurchased 5% of outstanding shares at attractive levels in the last 12-months.

Attractive valuation: In 2015, Berkshire Hathaway acquired Van Tuyl Group, the largest privately-owned automotive retailer with 100 franchises for $4.1 billion. Van Tuyl competed with Asbury and had a similar playbook. Terms were not disclosed, but we estimate Berkshire paid 7- 8x TEV/EBITDA. By comparison, Asbury trades around 8x TEV/EBITDA on the market’s bearish consensus 2023/2024 EBITDA estimates and a low double-digit free cash flow yield. Asbury has historically traded around 9-10x TEV/EBITDA, which we argue is still low given the company’s track record of capital deployment, operational efficiency, and organic growth initiatives (like Clicklane). We believe Asbury’s intrinsic value is at least 40% greater than its June 30 share price.

Playa Hotels & Resorts (NASDAQ: “PLYA”)

Playa Hotels & Resorts is a small-capitalization owner/operator of 25 all-inclusive resorts in Mexico (Cancun and Pacific Coast), the Dominican Republic, and Jamaica. Playa’s portfolio is branded (mostly Hilton and Hyatt), includes primarily luxury/upscale resorts, and operates at among the highest margins in the hotel industry. Playa’s resorts are irreplaceable assets in supply-constrained markets that continue to benefit from rising post-COVID international tourism.

We believe the public market discounts Playa’s shares based on recessionary fears, however, strong international flight data into Playa’s regional airport hubs do not support this view, and spot private market valuations for Playa’s hotels exceed its public market valuation. Management has demonstrated impressive capital allocation to address this valuation gap by moderating growth capital expenses for only the highest return projects and looking to sell select strategic resorts and repurchase shares at today’s attractive level. Over the last two quarters, Playa has repurchased more than 4% of the company’s outstanding shares. The company trades at a TEV/EBITDA of 7.6x (2023E), and a low double-digit free cash flow yield. We believe Playa’s intrinsic value is more than 50% greater than its June 30 share price.

White Brook Capital initiated what they’re calling a trading position in Unity Software (U), meaning they expect their holding period to be relatively short. That could make their thesis, which we share below, rather timely.

Unity Software Inc (U): We took a trading position in Unity Software during the quarter. A trading position is one where I expect the duration of the investment to be relatively short at the time of investment. During the first quarter, I completed much of the work and viewed Unity as attractive based on valuation, but decided to pass. Behind that decision were fundamental questions around corporate governance and the probability that Apple, at the unveiling of their headset, would either go alone in providing tools for developers to produce content for their new augmented and virtual reality efforts or also announce a wide settlement with Unity’s primary competitor, Epic Games, of all outstanding legal matters and a new partnership. Instead, Unity is being relied upon to help developers. Due to continuing concerns around their incentive plan and the strength of the board, it is unlikely that the position will prove to be a multiyear holding, but they are very likely beneficiaries of growth in artificial intelligence and virtual reality in the short term.

Unity theoretically benefits from several trends coming together at once.

1. Augmented and virtual reality were unveiled too early, they’re not permanent busts. Artificial Intelligence advances should improve automation efforts that make it easier for developers to produce more intricate and complex environments and games in three-dimensional space. Improvements in chip development, notably Apple Silicon, but also by competitive chip manufacturers like NVidia and AMD, should also improve playback and interaction of three-dimensional worlds.

2. Unity’s digital twin platform for producing digital versions of real objects is a competitive advantage. Their development platform is relatively easy to use and can be used across platforms as developers try to monetize, Apple, Meta, and any other competitive AR/VR platforms.

3. Unity’s ad network is important, both as a cash flow stream today for the company, but also for developers as they need to play a role in the chicken and egg paradigm seeding a new platform with an initially limited audience.

4. Epic Games’ lawsuit, the “bad blood” between the companies, and its partial ownership by Chinese giant Tencent, favors Unity in the US market.

I don’t expect White Brook Capital Partners to maintain a position over the long term, but we benefit from a good entry price and a positive backdrop.

Old West Investment Management sorted through the rubble of 2021 vintage SPACs and bought SmartRent (SMRT), a software and technology provider for multifamily owners and operators. They briefly detailed their thesis in their latest investment letter.

SMARTRENT, INC. (SMRT)

SmartRent is the leading smart home technology company focused on rental housing in the U.S. Multifamily owners and operators love their products which include smart access keyless entry, water leak detection and smart thermostats/climate control. They also offer self-guided tours for prospective tenants to see units, resident and staff management software and parking flow optimization. Based in Scottsdale, AZ, the company sells hardware devices and software that generates recurring revenue as they monitor their services.

At Old West, we are always looking for great owner/operators of companies to partner with. Lucas Haldeman founded SMRT in 2017 after serving as CTO at Colony American Homes, at the time a large owner of single-family rental homes. It was in that role that he realized the need for technology solutions to provide more efficient property management. Haldeman owns $15 million of SMRT stock, ranking him as the company’s largest shareholder.

Over the past five years SMRT has attracted the top multi-family operators in the country as customers, including the top seven apartment REITs. Invitation Homes, the largest owner of single-family rental homes, is one of SMRT’s 500+ customers. As far as competition goes in this space, SMRT has said they have more units deployed than all their competitors combined.

SMRT is rapidly riding the road to profitability. Revenue grew by 53% from 2021 to 2022 and forecast to grow by 43% in 2023 to $240 million. Gross and net margins continue to improve, and CEO Haldeman has repeatedly said they will be EBITDA positive by this yearend. The company has $200 million of cash on its balance sheet with no debt. SMRT went public in April 2021 as a SPAC at $10 per share. The share price quickly went to a high of $14 and then like most SPACs, dramatically fell to a low of $2.15 per share. Our average cost is $3.70, and it currently trades at $3.82. The market cap is $762 million, and the $200 million of cash equates to $1.00 per share.

To give you an idea of their growth potential, SMRT has installed 600,000 units and there are 45 million rental units across the U.S., and with no serious competition today it’s going to be exciting to watch SMRT grow.

Cove Street Capital discussed their newest position in Motorcar Parts of America (MPAA) with a brief recap of their thesis. Also, while not a new position, we also include their thoughts on SecureWorks (SCWX), a cyber security firm that boasts Dell as a 90% owner.

We recently initiated a position in Motorcar Parts of America (NASDAQ: MPAA). MPAA primarily remanufactures starters and alternators for large aftermarket auto parts retailers such as O’Reilly Automotive (Ticker: ORLY), Advance Auto Parts (Ticker: AAP), and AutoZone (Ticker: AZO). As common in the industry, MPAA entered into an accounts receivable discount program many years ago with their auto part retailer customers, and now as interest rates are rising, interest expense on these programs have tripled, causing a significant deterioration in earnings. MPAA has recovered some of the lost earnings through price increases, and due to nearly 50% share of the remanufactured starters and alternators market, we believe more price increases are to come. Also, the company has recently been capitalized by a private equity firm, Bison Capital, with a $32M convertible note that converts at $15 per share versus the current share price of $7. The additional capital could help MPAA consolidate other aftermarket auto parts manufacturers that are struggling with the current industry dynamics and increased interest expense.

SecureWorks (Ticker: SCWX) provides cyber security formerly as-a-service with an expensive in-house team of consultants and now has a software product called Taegis. SCWX is converting the entire business into selling only software and the conversions is almost complete. The next stage is to eliminate duplicative costs as they go from two business models to one. We expect solid growth within the cloud software business as they address a new customer world. Dell (Ticker: DELL) owns 90% of the company and thus the shares represent a "stub" in the eyes of many larger investors that like the idea and valuation but whine about the lack of liquidity. That can be a nice sweet spot for us in the longer run, but in the short run, the stock seems to us to have limited connection to its long-term value. We are holders but recognize we have been very early here.

Until next time! - EP

Looked at Playa, their debt load is crazy high compared to their cash flow, and this seems to be their best year yet.