EP109: Small Financials, Big Upside

Stock Ideas From Investment Professionals

Welcome, subscribers!

This week’s letters circle around a clear theme: overlooked financials with flexible models, aligned leadership, and serious upside potential. Whether it’s a microcap innovating in private equity, a fast-growing California bank with off-the-charts return metrics, or a low-multiple asset manager sitting on hidden value, the common thread is mispriced quality hiding in plain sight.

If you like under-the-radar businesses with proven operators and asymmetric setups, you’ll want to read this one closely.

We’re excited to share 4 deep-dive stock ideas, including:

• A multi-boutique asset manager trading at 3x EBITDA, with consistent buybacks and room for margin expansion.

• A misunderstood platform company scaling the search fund model—with blue-chip advisors and a track record to match.

• A community bank growing earnings 20%+ per year, with management owning over half the company.

• A small-cap lender with discounted loan optionality and a veteran CEO skilled at thriving in disrupted markets.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

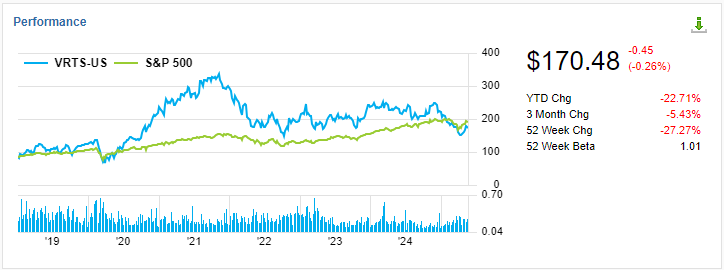

Gator Capital Management, a financials-focused fund with an impressive long-term track record, made the case for a re-entry into a former winner: Virtus Investment Partners (VRTS).

We believe Virtus Investment Partners offers a compelling investment from current levels. Virtus Investment Partners is a multi-boutique traditional investment manager. The company has several investment affiliates with their own investment teams and strategies. Virtus provides centralized sales, middle- and back-office services to support these teams. Virtus has grown by using cash flow to acquire additional investment firms. It keeps the investment teams of the acquisitions in place and centralizes sales and operations. We successfully owned Virtus for the Fund several years ago.

Our investment thesis is below:

1.High-Quality Business Due to Recurring Revenue and High Free Cash Flow - Virtus Investment Partners boasts a high-quality business model underpinned by recurring revenue streams and elevated free cash flow. The firm's strategic focus on asset management ensures steady income through management fees, which are largely predictable and stable. This recurring revenue is a testament to the company's robust client relationships and consistent performance, providing a strong foundation for continued growth. Furthermore, high free cash flow enables Virtus to reinvest in its business, pursue acquisitions, and return capital to shareholders, enhancing overall value.

2. Low Valuation on Price to Earnings and EV/EBITDA Basis - VRTS has an attractive valuation. It trades for 6.5x price-to-earnings (P/E) and a shockingly low 3.0x on Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization (EV/EBITDA) basis. VRTS has a strong balance sheet that matches the strong cash flow profile of the business. The company only has $100 million of net debt, which is about 0.3x EBITDA. In addition, VRTS carries a portfolio of seed investments in start-up funds and products valued at $140M. It recycles this seed capital into incubating new funds and products as existing seed investments payoff or fail. Virtus also has about $140M in CLO equity investments. These investments are made as its advisors form new CLOs. We subtract the seed investments and the CLO equity investments from Enterprise Value when we quote the 3.0x EV/EBITDA multiple. One could argue that seed investments and CLO equity investments are necessary to run the business. If we excluded these two items from Enterprise Value because they are necessary to run the business, we still calculate a very low 4.0x EV/EBITDA multiple. Virtus trades at a lower multiple compared to its peers

3. Low Debt Levels Provide Management Flexibility - The firm's prudent approach to debt management further strengthens its investment appeal. Virtus Investment Partners maintains low debt levels, which afford management significant flexibility to act on M&A or share repurchase opportunities. This conservative financial stance mitigates risk and enhances the firm's ability to sustain operations during economic downturns.

4. Potential for Earnings Accretive Acquisition - Virtus Investment Partners is well-positioned to pursue earnings accretive acquisitions. The firm's strong balance sheet and free cash flow provide the necessary capital to acquire additional investment management capabilities. Multiples for privately held investment management businesses are inexpensive. Virtus has a strong platform and history of integrating acquisitions to realize synergies and create value.

5. Consistent Dividends and Stock Repurchases – VRTS management has been consistent in returning capital to shareholders through dividends and stock repurchases. VRTS stock currently yields 5.6%. Stock repurchases further enhance shareholder value by reducing outstanding shares and increasing earnings per share (EPS). In Q1, VRTS management repurchased about 2% of the stock and signaled that they would be more aggressive given the stock price decline from early March. We would encourage management to consider increasing leverage by 1.0x EBITDA and repurchase 30% of the shares.

There are risks to our investment thesis on Virtus:

1. Challenged Flows Due to Active Management Out of Favor - Despite its strengths, Virtus Investment Partners faces challenges in asset flows, primarily due to the growing trend towards passive management. Active management has fallen out of favor with some investors, who prefer the lower fees and perceived simplicity of passive strategies. This shift poses a headwind for Virtus, potentially impacting on its ability to attract and retain assets. The firm must navigate this evolving landscape by demonstrating the value of active management and differentiating its offerings through superior performance and client service.

2. Some Past Acquisitions May Not Have Paid Off - Virtus's acquisition strategy, while generally successful, has not been without its missteps. Some past acquisitions have not delivered the anticipated returns. These underperforming acquisitions can weigh on financial results and erode investor confidence.

3. Waiting for Flows to Improve or Management to Take Action - Virtus Investment Partners is at a crossroads, awaiting improvement in asset flows or action from management to make an acquisition or materially increase share repurchases. This state of waiting creates uncertainty and requires patience from investors.

In summary, Virtus Investment Partners presents a compelling investment case with a robust business model, attractive valuation, low debt levels, and a clear commitment to shareholder returns. However, the firm must navigate challenges related to asset flows and past acquisitions. Investors should weigh these strengths and weaknesses carefully, considering Virtus's potential for growth and the strategic actions needed to address its current hurdles. With prudent management and strategic execution, Virtus Investment Partners could deliver substantial value to its shareholders over the long term.

3 more stock ideas are waiting for paid subscribers, including a fast-growing community bank and a search fund platform with blue-chip backing.

If you're in the business of identifying underfollowed compounders before the crowd, access like this isn’t a perk. It’s your edge.

Most of our professional subscribers expense their subscription through their firm as part of research or education. You can too. Just copy and paste the email below to your manager:

Hi [Manager’s Name],

I’d love to expense a subscription to Elevator Pitches, a newsletter that curates the best stock ideas from professional investor letters. It provides high-quality insights that help identify overlooked opportunities and special situations.

Here are two examples (here and here) of the types of posts they deliver each week. With a paid subscription, I’d gain access to every stock write-up they uncover.

Since Elevator Pitches serves as an educational and research resource, I was hoping it could be expensed through [Company Name]. The cost is just $90 for the entire year, which is a great value given the depth of insights provided.

Let me know if this is possible—thanks for your time and consideration!

Best,

[Your Name]