EP81: Dirt Movers

Stock Ideas From Investment Professionals

Welcome, subscribers!

We’re back with more investment ideas!

If you enjoy what we do, please consider forwarding to a friend or colleague who might also appreciate our work.

This week, we’re excited to highlight 6 new ideas, including:

A microcap highway & heavy equipment dealership roll-up

A small cap specialty distributor of niche products

A catalyst rich gaming equipment company in the midst of a break-up

Keep reading to learn more.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

Greenhaven Road Capital initiated a new position in Alta Group (ALTG), which they discussed at length in their latest letter. Like many COVID-vintage SPACs, ALTG has been a disappointment, but Greenhaven thinks Alta’s razor/razorblade business model combined with an attractive valuation make it an attractive opportunity today. Below are their thoughts.

NEW POSITION – ALTA GROUP (ALTG)

An investment thesis should fit into a paragraph, or in this case a sentence. For Alta Group, there is this nice sentence: This business is (1) less cyclical than it appears, (2) generates more cash than it appears, with (3) less debt than it appears, with (4) a significant hidden growing annuity type asset, and (5) run by an owner operator who can grow organically and through acquisition for the next decade-plus, at an (6) attractive valuation. Here is the not-so-nice sentence: When your $700,000 earthmover breaks down and your project is stalled, you are going to pay Alta Equipment Group a lot for the parts and labor to fix it because they have you by the…..

Alta Equipment Group is in the business of selling, renting, and, most importantly, maintaining heavy equipment. They own dealerships that have geographic monopolies for earthmoving equipment, environmental processing equipment, cranes, paving, and asphalt equipment. A couple of the brands you may have heard of are Hyster-Yale (forklifts) and Volvo (heavy construction equipment – not cars).

This is a razor/razorblade model, where the margins are low on the initial sale of equipment, but there is a long annuity-like service profit stream that typically accompanies the sale.

1) Less cyclical than it appears: Alta’s end markets are not the residential construction market, but rather infrastructure and warehouses, which are currently being supported by government spending and e-commerce trends.

While the new equipment sales certainly have a cyclical element, Alta’s end markets do appear healthy. The larger driver of earnings though, stems from their parts, maintenance, and repair segments which are far less cyclical. Yes, usage tends to go down in a softer economy, but these are non-discretionary purchases.

2) Generates more cash than it appears: The combination of continued acquisitions and GAAP accounting for rental fleets obscures the company’s cash-generation potential, which, in turn, makes the company screen poorly to computers. Acquisitions have totaled $440M over the last five years, opening new geographies and equipment brand types for the company to pursue further organic growth. However, as ALTG shifts the acquired businesses more towards a parts/services model post-acquisition, the real benefits of these acquisitions are only just starting to appear. Further obfuscating the cashgeneration potential is the current rental rate environment for their rental equipment business. Generally, Alta would be in a constant motion of selling portions of its rental fleet throughout the year while renting out the rest of the fleet out to maximize utilization. Historically, the used rental equipment has been sold for ~80-90% of the original cost paid. However, the rental rates the company can achieve today provide a more attractive opportunity than selling off portions of the fleet, which has the near-term impact of reducing cash flow from operations. If rental rates weaken, the company can revert to managing the fleet composition by selling more of the fleet and thus increasing cash flow. If rental rates continue to be strong, they are doing exactly what any long-term owners of the business would want—maximizing the opportunity.

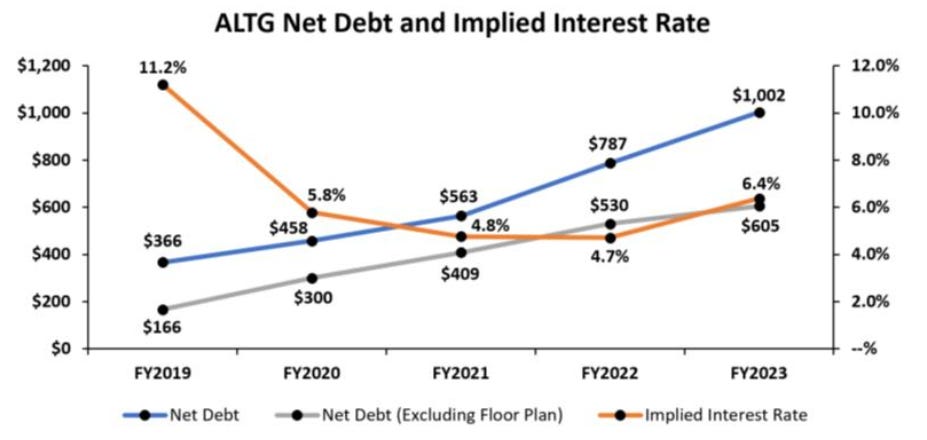

3) Less debt than it appears: The large data providers like FactSet show Alta Equipment Group with more than $1B in debt ($1,074). Of that amount, $397M is floor plan financing that is generally tied to the machines they have in inventory, is non-recourse to the parent, and can be cancelled with the return of the unsold equipment. We can argue about how to treat floor plan financing, but if you insist on calling it debt, it is a very, very favorable form of it.

4) Significant hidden growing annuity type asset: ALTG also has “sneaky” organic growth imbedded in its business model that the market does not seem to understand. The parts and services segment generates the most revenue and profits from previously sold equipment after the two- to three-year OEM warranty expires. Based on our analysis of SEC filings and pieced-together news articles, we estimate that cumulative equipment sales through 2020 were ~$2B. From 2021– 2023, the period in which equipment sold would still be under warranty, ALTG sold an estimated $2.4B of equipment. If we then build a waterfall of parts/services revenue coming online vs. the amount dropping off, we can clearly see the “sneaky” organic growth coming in at 11-12% per year going ahead, based solely on the equipment that was sold over the last three years. While any business operating in a cyclical industry can hardly be called inevitable, the organic growth tailwind inherent in Alta’s business probably comes pretty close.

5) Run by an Owner Operator with a long runway – Alta Equipment Group’s current CEO, Ryan Greenawalt, bought out his father and other family members in 2017. He currently owns ~18% of the shares outstanding, and a trust for his children owns another 5%. What started as a single heavy equipment distributor in Michigan 35 years ago has grown primarily through acquisition to 85 locations in the mid-west, east coast, and Canada. Fortunately for Alta Equipment Group, the pool of competing acquirers has been limited. The OEMs (Volvo, Hyster Yale etc.) limit the number of authorized distributors in specific geographies. The OEM’s also have to approve an acquirer and have historically shunned private equity backed entities. Thus the buyer pool can be small, and Alta Equipment Group is well positioned. Acquisition multiples are in the single digits of EBITDA and Alta Equipment Group can generally improve those economics with their focus on parts and services.

6) Attractive valuation – After dissecting the different components of the business and better understanding the capital structure, we get to a valuation that is compelling. After backing out of the floor plan financing, we are paying ~$980M for a business that is poised to earn $300-$400M per year of EBITDA over the next few years. While the gyrations of interest rates and the economy at large will impact those estimates to an extent, the variations should be increasingly muted as the more annuity-type parts and services revenue become a substantially larger portion of the overall business.

In 2023, the Free Cash Flow to Equity (FCFE) was $2.84 per share, up from $.74 per share at the time of IPO (de-Spac) 4 years ago, while the price has barely budged hovering in the $11-$12 range. If the free cash flow continues to grow and the share price does not, I would expect the company to be more aggressive with their buyback. As the largest owner, Ryan Greenawalt cares about share price and per share value and while cheap acquisitions are plentiful, we reach a point where ALTG shares are the cheapest.

There are 5 more ideas below for our paid subscribers.