EP79: Back In The Lab

Stock Ideas From Investment Professionals

Welcome, subscribers!

We’re back with another batch of investment ideas!

If you enjoy what we do, please consider forwarding to a friend or colleague who might also appreciate our work.

This week, we’re excited to highlight 8 new ideas, including:

A pioneering company in the life sciences sector, known for its revolutionary contributions to mRNA technology and cancer vaccines. This firm has exhibited exceptional growth potential and unique market positioning, bolstered by its innovative products and strong leadership.

A leading player in the bioprocessing industry, recognized for its single-use bioreactors and superior customer relationships. This pure-play company's comprehensive portfolio and industry dominance make it a compelling investment, especially given its strong market share and growth trajectory.

A top equipment rental company in the US with significant presence in the Sun Belt region. This firm is well-positioned to capitalize on infrastructure investments and industry consolidation, offering substantial upside potential through its strategic acquisitions and pricing power.

Keep reading to learn more.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

RGA Investment Advisors discussed two new positions in their recent client letter, both in the life sciences space. We include their thoughts on Maravai Lifesciences (MRVI) and Sartorius (SRT-DE) below.

MARAVAI: MARGINS + SAFETY = MARGIN OF SAFETY

We first purchased shares of Maravai early in Q3 of 2023. Much like our experience with META in 2022, almost immediately following our first purchases, the stock’s price tumbled. Given Maravai is a small cap, with a fairly illiquid float and volatile shares, we started our position on the smaller side. As the stock continued to stay weak, we used this as an opportunity to meaningfully increase our holding, much as we had done with META.

Maravai first hit public markets in late 2020 on the heels of its phenomenal success in helping the Pfizer/BioNTech mRNA vaccine approach commercial launch. Maravai was formed as a holding company backed by private equity firm GTCR. Its two key subsidiaries are TriLink Biotechnologies and Cygnus Technologies, in the Nucleic Acid Production (NAP) and Biologics Safety Testing (BST) segments respectively. TriLink is the subsidiary whose capabilities formed a critical piece of the Pfizer/BioNTech vaccine, while Cygnus is one of the most important quality control companies for the manufacturing of biologics. Each is an incredibly unique asset.

TriLink is the primary asset in the NAP segment, holding critical patents and capabilities for the research, development and commercialization of mRNA. CleanCap is the company’s flagship product line that made the BioNTech vaccine possible. Prior to TriLink’s development of CleanCap, researchers had to use a process called enzymatic capping. Enzymatic capping remains in use; however, it is far less efficacious than CleanCap and in terms of all-in cost it is significantly more expensive to deploy. Capping is critical for mRNA in both nature and in vaccine or therapeutic applications. The cap is the piece that protects the mRNA itself, helps signal the cells that it is ready to make a protein, and facilitates the mRNA’s movement within the cell. CleanCap is a patented reagent for capping mRNA in a way that most closely mimics nature itself, allowing for a much simpler manufacturing process (one step vs multiple) and superior protein expression.

Over time, via acquisition and development the company has broadened its capabilities around CleanCap to add a portfolio of enzymes and reagents, as well as a full-suite CDMO that can take a biotech customer from preclinical all the way through cGMP manufacturing. Maravai’s new CEO, William “Trey” Martin (a hire from our portfolio holding Danaher), has been expanding the vision beyond mRNA applications itself to “programmable medicines,” which includes CRISPR gene editing.

NAP revenues soared with the rapid deployment of COVID vaccines around the world and then collapsed as the pandemic shifted farther into the rearview mirror. Importantly, the core business of TriLink continued to grow and the vaccine itself served as critical validation of what had formerly been largely theoretical and experimental applications. This opened the path to an accelerating rate of study and entry into clinical stage experimentation across the biotech industry. Although there is some negative public opinion about the COVID vaccines themselves, the science is now provably validated and applications for mRNA technology range well beyond COVID and then flu or RSV vaccines, to potential curative treatments for some of the most deadly forms of cancer.1 Cancer “vaccines” of this kind would be a gamechanger for humanity and an important propellant for Maravai’s business prospects, considering they would use considerably more Maravai content per treatment than does the COVID vaccine.

Cygnus, within Maravai, is a hidden gem. At peak COVID revenues it was a fairly insignificant portion of the business and to the average person looking at the stock, appeared a mere afterthought. With COVID vaccine-related revenues collapsing, its revenue contribution on a quarterly basis rose to around a quarter of the business towards the end of 2023 (and 22% for the full year). Yet, the focus remains far higher on TriLink due partly to its world-changing potential as well as its continued greater contribution to the business itself. We think Cygnus alone is the kind of asset that could conceivably fetch more than the company’s entire market cap at the stock’s lows in the past year. Cygnus is the industry-leading quality control testing kit that simplified and disrupted quality control for the development of monoclonal antibodies and is spec’d into all 21 of the FDA-approved CAR-T therapies. Cygnus led the BST segment to $64.2 million in sales in 2023, generating $46.9 million in EBITDA, a whopping 73% margin. Cygnus was built over years with little incremental capital or opex required and given this revenue scale, margin structure and dominant spec’d in position would generate considerable interest were it ever to hit the auction block.

As for Maravai as a whole, the company’s margin structure is perhaps the best we have ever seen. At peak COVID revenues, the company reported EBITDA margins upward of 70%. Despite losing about 2/3rds of their revenues from 2022 to 2023, the company still delivered 22.6% adjusted EBITDA margins. Maravai did this in an environment where COVID winners turned losers were fighting just for a chance to become profitable within the next few years. Meanwhile, towards the end of the year, the TriLink business stabilized and the path to regaining a robust growth trajectory and recouping lost margin emerged. At our average price between our Q4 2023 and Q1 2024 buys, we paid a low-teens multiple for what we think the company will deliver in 2026 EBITDA. Importantly, 2025 to 2026 are the years where the aforementioned progress of pushing mRNA treatments into the clinic should manifest in graduating more vaccines and therapies through the FDA process. This means that our low teens EBITDA multiple at prices paid should come with growth rates upwards of 20%. Although we never underwrite to multiple appreciation, we think this is a situation where it is far more likely to happen than not for two elite assets, with other-worldly margins wrapped in one company.

SARTORIUS: PURITY IN THE PURE PLAY OF BIOPROCESSING

In our Q3 2023 commentary, we featured a section on our investment in Danaher entitled “Purity in the Crown Jewel of Bioprocessing.” Specifically, we were speaking to Cytiva, Danaher’s bioprocessing business formed by the merger of Pall Corp and GE’s bioprocessing division. We will not repeat the features that attract us to bioprocessing in general, nor the elements of timeliness, though we will emphasize that our confidence in timeliness has actually increased since writing that piece. While Danaher has performed admirably ever since, its peer Sartorius, which was referenced by labeling bioprocessing “an oligopolistic market, with a small number of critical players and extremely high barriers to entry.”

Although Danaher owns the crown jewel of the industry, only Sartorious amongst these peers is what can be described as a “pure play.” At Sartorius and its Sartorius Stedim (publicly listed in France as a stub company) subsidiary, bioprocessing is essentially the business. Sartorius boasts a comprehensive portfolio for bioprocessing, covering the upstream, downstream and media; however, its largest and most lucrative business is in the “upstream” flow. Upstream is where a small a cell line is taken, scaled from very small quantities to much larger ones and then harvested, before they are purified, separated and isolated into the “end product” downstream. Sartorius is a world leader in single-use bioreactors. These are smaller-scale bioreactors than the traditional steel ones that use replaceable plastic bags, within which the scaling takes place. Sartorius dominates single-use from the research phase through the commercial phase. For example, the AMBR is an industry-leading offering at the smaller end of the spectrum, which helps Sartorius gain critical share in the research stages and in Cell and Gene Therapy applications. This dominance in research phases helps secure spec’d in placements come time for commercialization, while the CGT placement supports the more demanding, but smaller scale needs of the next frontier of the biotech industry.

Beyond the share capture of single-use, we want to highlight a few unique qualitative traits. We have spoken to numerous customers who have emphasized Sartorius’ unique relationship with their customers. Several even went as far as using the word “partner” as a result of the level of service Sartorius’ field team delivers. They have an “Innovative Differentiated Solutions” team who help customers from process design and equipment placement to clean room designs. These services are offered in pursuit of equipment sales and go above and beyond any peer in the industry who customers view favorably, though in a more mercenarial way. Moreover, even during the tight supply chain environment of COVID, Sartorius was viewed as the most reliably on-time and consistent solutions provider. While others in the industry have tried to copy Sartorius’ service-first mentality, none have come close to delivering on it or fostering the kind of relationship that Sartorius has with their customers. We think this mentality, beyond the share gains of single-use generally, has resulted in impressive share gains over the past decade and provides the right to win further share (and grow faster than this fast-growth industry) over the next decade.

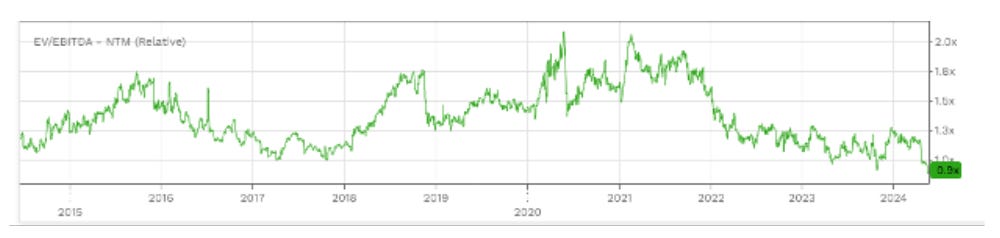

Typically Sartorius trades at a decent premium to Danaher due to its pure play status in the highest growth area of the industry and its relatively higher growth rate given the share single use bioreactors are taking from stainless steel. Despite relative growth remaining favorable during the downturn and looking to continue so on the way out, Danaher’s meaningful outperformance has created a unique valuation spread:

We started buying Sartorius in the first quarter and will note that we purchased even more recently as Sartorius’ valuation dropped beneath that of Danaher’s (equal valuation would be 1.0x in the chart above, with any number above 1.0 representing Sartorius’ boasting a higher valuation and less than 1.0x representing Danaher with a higher valuation). Sartorius trades at a mid-teens EBITDA multiple on our 2025 estimate and our now average price.

This week, we have 6 more stock ideas for our paid subscribers.