EP54: The Eyes Have It

Stock Ideas From Investment Professionals

Welcome, subscribers! Today, we share pitches for a small cap bank, a mega-cap biotech, and a Canadian infrastructure company.

Read on to learn more. 📕👇

Your support is appreciated. If you enjoy this issue, please forward to a friend or colleague!

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

Bronte Capital went into detail on the firms’s largest position, Regeneron (REGN), in their most recent investor update. Can the company overcome a recent Complete Response Letter from the FDA? Bronte discusses that and more below.

Regeneron

As explained in our June 2021 letter, Regeneron is a drugmaker who combine their ability to humanise the mouse genome and the largest genomic database in the world to develop new medicines, particularly monoclonal antibodies. The general public probably best knows them for the (then) experimental antibody cocktail given to President Trump when he had COVID-19, however their drug development record is far more extensive.

Historically the core drug at Regeneron is EYLEA – a drug injected into the back of the eye to treat wet age-related macular degeneration (AMD), the leading cause of blindness in old people. EYLEA is one of several VEGF inhibitors that have dramatically reduced the cliché of “old-and-blind”. For over a decade, EYLEA has been the preferred anti-VEGF treatment mostly owing to its less frequent dosing vis-à-vis other agents (it is typically taken once every eight weeks). It has been injected nearly 60 million times into peoples’ eyeballs since it was launched. Because blindness in old people is very expensive (think of the care costs), and EYLEA has significantly decreased the treatment burden for patients with wet AMD, Regeneron has been able to charge a lot for the drug. In Australia it is amongst the biggest single costs in our socialised pharmaceutical purchase scheme.

There are however other drugs – most notably Dupixent – a drug discovered by Regeneron, developed largely at Sanofi’s expense and hence half owned by Sanofi. This deals with a wide range of type 2 inflammatory diseases, including atopic dermatitis, and if all goes well will wind up being one of the largest drugs in the world by revenue (probably behind the GLP-1 agonists). Beyond that, there are other important drugs such as Libtayo, which effectively unblocks the immune system’s response to certain types of cancer. Regeneron plan to mix-and-match Libtayo with a wide range of other anti-cancer agents, and expect it to generate lots of revenue as these programs bear fruit.

The last year has been mostly extremely good for Regeneron with several pivotal trials producing very compelling results leading to actual and probable label expansions for Dupixent and other drugs across the portfolio. Perhaps the most important result was in March 2023. Regeneron and Sanofi announced phase 3 results which demonstrate Dupixent’s ability to treat chronic obstructive pulmonary disease (COPD). This is the first new approach to COPD in over a decade and is a potentially enormous market. By some measures COPD is the third leading cause of death worldwide. Dupixent is already a drug with over $10 billion revenue. It can and should be much larger.

However, the overwhelming issue with Regeneron as far as the market is concerned is that EYLEA is nearing the end of its patent/market exclusivity and is expected to face increased competition from various branded/generic agents. In the last decade, many attempts have been made to beat EYLEA’s dosing frequency but have generally not achieved the same visual gains.

Over several years, Regeneron developed a higher-dose formulation of EYLEA (aflibercept 8 mg) with the aim of reducing the treatment burden even further while maintaining the safety and efficacy of the original drug. According to the company, the drug was very difficult to formulate as the protein is viscous and must be injected into the eye.

In two pivotal trials, aflibercept 8 mg demonstrated that the vast bulk of patients on an 8- week EYLEA dosing regimen could be rapidly moved to, and maintained on, a 12 or 16-week dosing regimen using the high-dose formulation, with no change in efficacy or safety. Many of the patients in these trials achieved as low as two doses of the high-dose formulation each year. At this point, aflibercept 8 mg appears to have a truly best-in-class profile with patent protection that could last for many years to come. High-dose EYLEA should reduce the (considerable) costs of administering the drug, increase the overall safety and convenience of an anti-VEGF treatment regimen for a patient (by requiring fewer injections each year), and might improve compliance (thus reducing the number of blind people who need care). Regeneron should be able to charge for that.

Alas not all has gone well. Late in June, the FDA issued a “Complete Response Letter” to Regeneron in relation to high dose EYLEA. A Complete Response Letter is usually, though not always, a total rejection which means the drug will never see the market and stocks fall very sharply on Complete Response Letters. Immediately Regeneron became our biggest detractor in the quarter. This stresses us only a little.

According to the company, the rejection was “solely” due to an ongoing inspection at their contract syringe filler (which is now known to be Catalent), and the FDA did not identify any concerns with the drug substance itself, or the design of the pivotal trials. Our judgement is that Regeneron management have told the truth in the past – both positive and negative - and that they are telling the entire truth in this case.

If it is just a manufacturing issue the drug should be approved this year though we do not know when. Manufacturing issues with syringes that are injected into the eye are serious. Any mistake in sterility or otherwise would likely involve the client going blind – an unacceptable outcome.

Furthermore we believe Regeneron’s profit share from Sanofi will grow quickly, driven by Dupixent. Libtayo’s recent cancer approvals are a bonus.

As long as EYLEA sales don’t fall of a cliff prior to the high-dose version being available then Regeneron’s profits should continue to rise. And that is before a pipeline arrives that we think is very promising.

There is a question as to whether we should buy more Regeneron – but there are two concerns.

a) We are already very large in the stock.

b) There is a nightmare scenario where the manufacturing issues at Catalent for high dose Eylea also infect the current low dose product. This scenario is unlikely but would result in the new competitive products getting a large foothold and would thus sharply reduce medium term Regeneron profits.

Gator Capital Management is a financials-specific investment manager. This quarter, they detailed an opportunity on the long side in Old Second Bancorp (OSBC), a $650 million market cap regional bank headquartered in Illinois. We include their thoughts below.

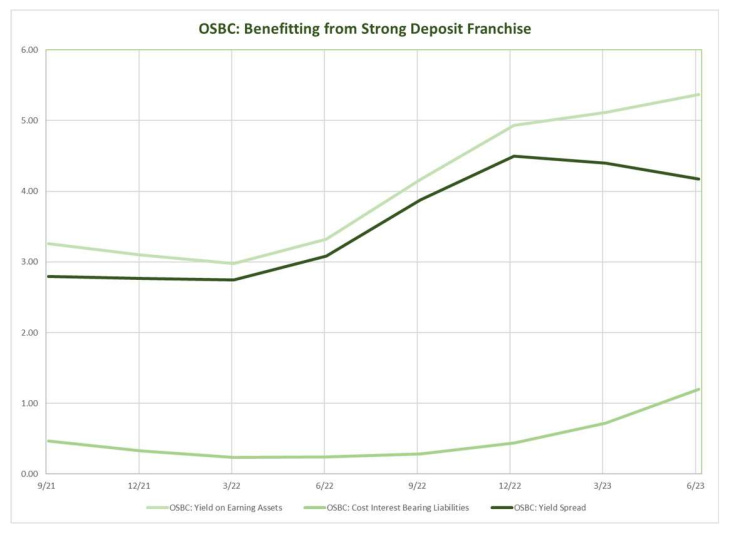

Old Second Bancorp is a commercial bank in the far western suburbs of Chicago. Old Second is valued at 1.4x tangible book value. Old Second is well positioned for the current high short-term interest rate environment. In 2021, Old Second acquired West Suburban, which was focused on suburban markets between Old Second’s branches and downtown Chicago. West Suburban had great branch locations in DuPage County that the former CEO had purchased in the 1950s and 60s. These branches create a very strong core deposit franchise with long-term customers. Over the past six quarters, Old Second’s net interest yield spread has risen from 2.77% to 4.17% as earning yields on loans and securities have risen and the deposit franchise remains stable with funding at relatively low rates. We can see the increase in net yield at Old Second in the graph below. The light green line at the bottom of the chart shows the cost of deposits low and rising gradually. Rising asset yields have outpaced rising deposit costs until the most recent quarter. The dark green line is the net yield which has risen. Admittedly, the net yield will not expand from current levels, but continued asset repricing should offset further increases in deposit costs.

Old Second had a minor hiccup with some of the loans they acquired in the West Suburban acquisition. We have gone through the loans with management and believe these are ring-fenced and reflect the more conservative credit culture at Old Second vs. West Suburban.

We can see upside for Old Second to at least 2x tangible book with high book value growth in the next few years.

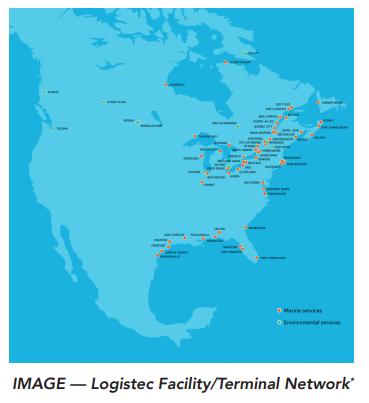

Alluvial Capital Management meaningfully increased its position in Logistec Corporation (LGT.A-CA). Logistec operates terminals at many ports throughout Eastern Canada. Alluvial thinks the shares are worth in excess of $100, which is ~50% above its current price. They discussed the company in their recent letter, which we include below.

Our most significant newish holding is Logistec Inc. The fund has maintained a small investment in the company for a few years now, but I elected to increase our holdings meaningfully in response to a promising development in May.

Logistec is one of Canada’s most successful public companies. It has the extraordinary distinction of being profitable every year for 50+ years, with no indication the streak is about to end. Logistec’s main business is operating terminals at dozens of ports in Eastern Canada and the US. Simply put, this is a great business. Logistec enjoys strong pricing power and consistent demand for its services. Logistec’s other segment is a profitable environmental services business that remediates polluted industrial sites and aging municipal water systems.

Despite its track record of profitability and growth, Logistec struggled in recent years to attract the market’s attention. Despite nearly doubling its earnings since 2018, its shares would not move. The company tried various means of highlighting its successes. It initiated quarterly earnings calls and published an investor presentation for the first time. No luck. The company was simply too small and its shares too illiquid for the market to capitalize the company properly in the short run. So in late May, Logistec’s controlling shareholder (a company controlled by the daughters of the founder) contacted the board of directors to inform the company it was seeking a means of disposing of its shares. The company responded by initiating a sales process.

I believe Logistec shares are worth in excess of $100 and that the company will achieve a sale price of at least $90 per share. This would represent a multiple of 10x 2022 EBITDA and ~9x 2023 EBITDA, accounting for a recent acquisition and improving results at both company segments. There is a strong appetite for port-related assets from infrastructure investors and pension funds. (Indeed, the Caisse de Depot et Placement du Quebec is a large existing holder of Logistec shares and is surely kicking the tires.) The presence of the smaller, less attractive environmental services business is a complicating factor, but a separate buyer can no doubt be found if necessary. While the timeline is uncertain, I would expect an announcement of some type before year-end. Even if no deal materializes, downside is limited by Logistec’s modest valuation and the knowledge that the company is for sale. The fund was an enthusiastic purchaser of Logistec shares in the $50s. I remain very confident in our investment as shares sit at $65.

Until next time! - EP