Welcome new subscribers!

We have 6 new ideas to share with you this week.

If you find these pitches interesting, please forward to a friend or colleague.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter if you’d like to be included in a future issue.

Let’s get to it.

L1 Capital International Fund reiterated their thesis for Amazon.com, Inc. (AMZN), one of the fund’s largest positions.

Amazon.com – so what is going on?

“You shouldn’t own common stocks if a 50% decrease in their value in a short period of time would cause you acute distress.” – Warren Buffett

Easier said than done, Mr. Buffett! The share price of Berkshire Hathaway (Buffett’s investment group) has fallen 50% multiple times. So Amazon’s 50% share price decrease in 2022 has laudable historical company. Nor is this the first time Amazon’s share price has fallen over 50% since its public listing. It doesn’t make the situation feel any better.

So, what is going on? Why has Amazon’s share price halved over the past 12 months and under-performed weak equity markets?

As outlined on page 5, investors are concerned with four key issues:

▪ Macroeconomic pressures on consumer ecommerce spending,

▪ Elevated costs impacting both Amazon’s ecommerce business and Amazon Web Services,

▪ Slowing in the growth of Amazon Web Services (AWS), and

▪ Shift away from higher growth technology businesses.

Macroeconomic environment

There is no denying the macroeconomic environment has deteriorated during 2022 and Amazon faces more challenging operating conditions, as do most businesses. Amazon is the leading ecommerce business in the U.S. and many international markets, excluding China, generating well over $400 billion of revenue, excluding AWS. A slowing in consumer (and business) spending will naturally flow through to Amazon. Amazon is also cycling elevated activity caused by COVID-19. As the world continues to normalise, consumers are returning to physical shops and ecommerce penetration of retail sales is adjusting back to historical trends at a faster rate than expected. Amazon’s growth rates will also slow because of the law of large numbers. We have allowed for realistic growth in our base case and see upside if the economic environment improves.

Elevated costs

Anyone who has run a business will tell you it is usually better to have a costs problem than a revenue problem. From our perspective, Amazon’s revenue growth has not been particularly disappointing, but the growth in costs and resultant pressure on margins has been greater than our expectations. Cost pressures are evident at many levels – higher cost of goods impacting gross margins, increased fuel and energy costs, infrastructure inefficiencies following a period of rapid expansion and increasing labour costs which impacts all aspects of Amazon’s integrated operations.

Employees and employee costs

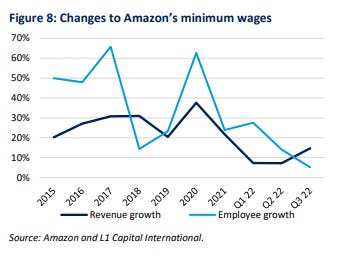

Over the past 7 years, Amazon’s total revenue has increased from around $100 billion to around $500 billion, a staggering 25% cumulative average rate of growth (CAGR) for some very large numbers. Employee numbers have increased even faster, from 230,000 to over 1.5 million, equating to a 31% CAGR (see Figure 8).

Amazon added 500,000 employees in 2020 and a further 300,000 employees in 2021 as it scaled up to meet rapid growth during the pandemic and to support international expansion. In recent times Amazon’s revenue growth has slowed off a very high base, with revenue from sale of goods online essentially flat. In short, Amazon over-hired and is progressively adjusting its employee base to increase productivity. Recently, Amazon confirmed 18,000 redundancies concentrated in its Amazon Stores and People, Experience and Technology divisions.

While we do not expect redundancies in the people-intensive warehouse and transportation areas, we do expect thoughtful replacement of natural attrition and ongoing productivity efficiencies. There are already early signs of tangible action with total employee numbers drifting down in 2022.

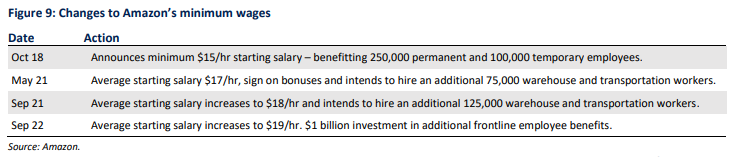

Amazon’s labour practices are far from perfect. That said, Amazon has been at the forefront of increasing minimum wages in the U.S. As illustrated in Figure 9, Amazon has supported a minimum starting salary of $15/hour since 2018, and its current average starting salary for warehouse and transportation workers is around $19/hour. The U.S. Federal Minimum Wage is still stuck at 2009 levels of $7.25/hour.

Share-based compensation

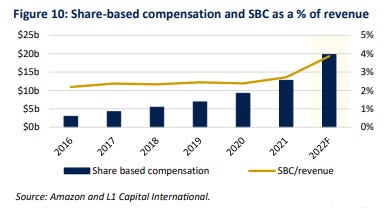

The growth in Amazon’s share-based compensation has materially exceeded our expectations and has been a major disappointment, meaningfully lowering our valuation of Amazon. We recognise Amazon needs to pay competitively to attract and retain the best talent, particularly in the Amazon Web Services division, and that Amazon’s sharebased compensation structure had some particular quirks which led to adjustments in 2022. However, the increase in share-based compensation by an estimated $7 billion in 2022, rising to around 4% of total revenue compared to the low 2s in the past substantially lowered our near-term earnings expectations for Amazon and our valuation of the business (see Figure 10). With almost daily announcements of layoffs by technology companies, including Amazon, it is highly likely we are past the immediate peak in technology employment costs. We do not expect Amazon’s SBC expense to reverse, but we do expect stability going forward.

Shipping and fulfilment costs

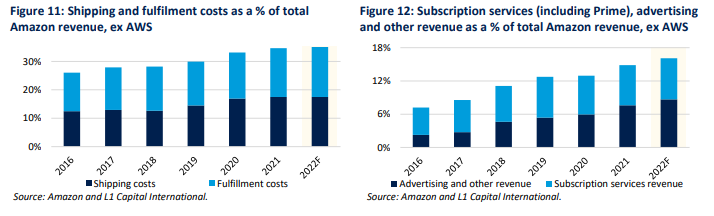

Higher fuel, freight and employee costs, operating efficiencies and increasing service levels have been reflected in an increase in Amazon’s shipping and fulfillment costs. These costs as a percentage of Amazon’s total revenue, excluding AWS, have increased from around 26% of revenue to 35% of revenue over the past few years, despite sustained outsized growth in advertising and subscription revenue which have no shipping or fulfillment costs (see Figure 11 and 12).

We estimate Amazon’s cost to fulfil and ship an online unit has increased over 40%, despite a nearly five-fold increase in volume of units fulfilled over this period. We expect a gradual improvement in operating efficiencies as Amazon beds down the massive expansion in its fulfillment and logistics network over the past few years.

Specifically, Amazon management has commented that 2022 capital investments are expected to be around $60 billion, similar to 2021. This allows for a reduction in fulfillment and transportation capital investments of approximately $10 billion compared to 2021 to better align expansion projects with demand, offset by an approximately $10 billion year-over-year increase in technology infrastructure, primarily to support the growth of AWS.

Amazon Web Services (AWS)

AWS is one of the highest quality businesses in the world. In less than 10 years, AWS has developed into a business generating revenue of $80 billion and operating profit of around $23 billion. Outside of China, only Microsoft through Azure, and to a lesser extent Alphabet’s Google Cloud Platform are the only credible competitors. Technology, scale and capital requirements are strengthening barriers to competition, while cloud computing has an extensive runway for further growth.

2021 was an exceptional year of growth for AWS. Despite an ever-increasing base, AWS increased revenue by $17 billion or 37% to $62 billion, and maintained operating margins at around 30%.

We still expect robust growth by AWS, but the business is not macro immune and will also be impacted by a slowdown from customers in the technology sector, particularly less established businesses. Amazon is likely to exit 2022 with a growth rate around 20%, still exceptional, but a slowdown from recent levels and a further tapering of growth rates is likely over time.

Operating margins are a more complicated discussion. Amazon (along with its peers) has increased the useful life of equipment in its data centres, lowering depreciation and increasing operating profit. This contributed to operating margins spiking to 35% in Q1 2022. Subsequently Amazon increased share-based compensation, which was particularly targeted at AWS, reducing operating margins below 30%. Q3 2022 operating margins were further impacted by a softening in operating conditions and increased energy costs. We expect AWS’s operating margins to gradually increase from current levels, which is moderately below our prior expectations.

While AWS’s operating performance is only modestly below our prior expectations, some analysts and investors had, in our view, unrealistically high expectations. Negative revisions to expectations have contributed to negative sentiment impacting Amazon’s share price.

Missing profitability

Excluding AWS, Amazon will report an operating loss in 2022. Notwithstanding the cost pressures outlined and likely substantial losses in less mature international operations, our analysis suggests Amazon is making significant losses on initiatives that are not core to Amazon’s existing operations – initiatives like Project Kuiper (satellites), Zoox (autonomous vehicles), Health, Alexarelated AI projects and video games. Experimentation and side developments are core to Amazon’s culture and have led to AWS and other significant businesses. However, we believe investors would benefit from Amazon disclosing the size of investments in these initiatives and increasing cost discipline, a process that has likely already commenced.

Summary

Amazon is an immense and complicated group of integrated businesses, generating around $500 billion of revenue and employing over 1.5 million people. Yet, fundamentally, it is powered by two key drivers – ecommerce and cloud computing. Amazon and AWS are both global leaders in ecommerce and cloud computing, respectively, and are increasing their barriers to competition. Amazon is facing cost pressures and the macroeconomic environment has worsened. Interest rates have increased dramatically which does lower the value of future earnings. Accordingly, we have reduced our valuation assessment of Amazon in 2022, but not enough to justify a 50% fall in Amazon’s share price.

We do not expect any silver bullet or quick fix to drive a rapid recovery in Amazon’s profitability, and future expectations need to be set at realistic levels. We remain confident in Amazon’s management and note meaningful actions have already been taken to improve operating efficiencies and enhance longer term shareholder value. In our view, Amazon’s share price has been oversold and offers compelling value. So far in January 2023, at the time of finalising this report, Amazon’s share price has increased by 17%. There is substantial further upside before Amazon’s share price approaches fair value.

Tourlite updated their thoughts on Perimeter Solutions (PRM) after its recent sell-off. Perimeter, for those unfamiliar, counts Nick Hawley (Chairman of TransDigm) and Will Thorndike (author of The Outsiders) among its management team.

Long: Perimeter Solutions (PRM)

Perimeter is the sole qualified provider of aerial fire retardant for many applications. This mission critical product represents a small portion of its customers’ spend, and revenue is recurring in nature as long-term secular tailwinds (growth in number and size of fires) support growth. Perimeter is led by what we consider to be an experienced, best-in-class, capital allocation focused management team.

Perimeter checks our boxes for an investment. It is a market leader in a growing market, strong cash flow generation and return on capital, talented management team, trading at an attractive valuation.

On December 12th, Morgan Stanley published a note from management’s road show:

“PRM's major competitive moat in its core market remains its greatest value proposition — and the greatest investor debate... Near term, it seems likely that Fortress (the potential entrant) will reach full qualification for usage by the US Forest Service in 2023. However, this will likely carry more headline than practical risk. The real point of contention is whether it is logistically efficient for firefighting agencies to use multiple, non-compatible fire-retardant solutions.”

Perimeter’s shares sold off over 10%. We agree that the risk is more in the headline than risk to the underlying business and market share.

We believe there are a few reasons the stock continues to trade where it does today:

1. Concern over the approval of a potential competitor's product for aerial use

The risk of a competitor taking market share is unlikely. Perimeter is currently the only supplier with USDA approval. While it is likely Fortress will be approved in the near-term, Perimeter’s infrastructure and integration into the supply chain provides a lasting competitive advantage to help maintain market share. This, combined with the fact that Perimeter’s product represents only ~3% of customers suppression spend, makes it challenging and unlikely for Federal and State agencies to switch providers.

2. Variability in earnings as a result of variation in fire season

We understand fire seasons are not perfectly linear but the overall trend in acres burned continues to support unit growth. We believe there was some misunderstanding of the fire suppression market this year. This year’s fire season had a large number of acres burned in Alaska. Since fire retardants are not often used in remote locations where the fire is not a threat to humans or infrastructure, this did not provide support to Perimeters volumes.

3. Some investors are turned away by unique compensation structure

In our view, if it’s a clearly defined plan and you can model it out, you can account for it going forward. We like a management team that is paid to perform and has skin in the game.

Revenue should be able to compound around 10% from a combination of increased volumes and mid-single digit price increases. Volume growth will be fueled by continued increases in acres burned, larger fires, and further stretched out fire seasons. Outside of its North American Fire business, additional growth should come from underpenetrated international markets and the Specialty Products segment. International is currently around 20% of revenues and gaining traction. The second leg of Perimeter, which gets less focus and represents 1/3rd of revenues, is Specialty Products which, as of the third quarter, has grown year-over-year revenues 40% and has more than doubled EBITDA.

Based on our 2023 projections, at the current share price of around $9, Perimeter is trading around a 6% free cash flow yield. That is for a business with considerable competitive advantages that should grow free cash flow per share by over 25% per year for the next two years at least. This is a business mostly uncorrelated to economic cycles and we believe there is limited downside to normalized earnings. We see a path to near $1 per share of free cash flow by 2025.

Like with many funds, White Brook Capital used their 4Q investment letter to reevaluate a position that has (so far) not worked. Their updated thesis on Greenbrier Companies (GBX), a railroad car manufacturer & leasing company, is given below.

Every major drawdown in an individual security at White Brook triggers a First Principles review. A First Principles review means that prior convictions and prior theses statements are disposed of and the investment thesis is rebuilt from the ground up. This occurs even when the portfolio outperforms the market, like it did this year. In 2022, the main detractors to performance were investments in a railcar supplier and in an investment firm that masquerades as a bank, both triggered reviews, the former I’ll detail here. I believe both underperformers should reverse during 2023 and beyond.

Today, the Greenbrier thesis is slightly different from what it was before the review with increased conviction around a couple points. For practitioners, the Greenbriar thesis is two fold, over the next couple years, the company has significant tailwinds to operationally revert. Secondly, the company is using its excess cash flow to invest in a structurally advantaged leasing fleet that will improve the regularity of its outyear cash flows. In many ways, the company is doing an as-a-service conversion in the industrial sector, building a low-risk, secured, better yielding, commercial bank operation while also being one of two large-scale suppliers of railcars to the railroad and shipping industry. In three years, the company should generate more free cash flow at a higher return on invested capital and with much increased regularity.

Having endured a significant decline, meant that the The First Principles review for Greenbrier Companies, Inc needed to more expressly confirm each of those points or prove another thesis altogether to remain in the portfolio. It resulted in increased conviction based on three points.

1.Demand is solid. Currently, few railcars are in storage, and the ones that are in the words of one expert, “are for a reason”. Railcars are 40-50 year assets, the oldest of which date back to the deregulation of the railroad industry. Current demand for this year and forecasted demand for the next 3 years, is entirely replacement demand for cars reaching end of life. Even taking into account that each railcar’s capacity has grown by 15% and therefore can shrink count by the same, the next 3 years of demand, only replacing those that are aging out, is likely to result in compounded year over year growth. In 2023, aided by the Freight Railcar Act of 2022, backlogs are likely to fill, providing for plannable and fillable demand. Because two large players dominate the industry, and demand is unfillable in the near term by the industry at large, evidence that textbook Cournot pricing dynamics - which allows firms to maximize profit - are occurring.

Current forecasts do not include any benefit from US reshoring manufacturing broadly nor do they account for railroads taking share from trucking. They do account for increased operational efficiency by the railroad companies (resulting in needing fewer cars). Should either of the positive developments occur, another leg of growth in the outyears is likely to occur and should railroad service levels continue to struggle - that would prove a mild positive to demand.

2.Greenbrier’s leasing operation is best in class and the foundations were built by the same person who previously built the other best in class leasing operation. Greenbrier began its leasing operation in 2021 by partnering with Longwood Group, run by Stephen Menzies, the former President of Trinity’s railcar leasing group. Greenbrier’s fleet has similar best in class operating metrics to Trinity’s, a similarly advantaged operation with first priority on Greenbrier’s output and a broad repair shop presence, and best in class leasing rates and usage.

3.Margins should increase significantly. During 2022 Greenbriar relocated significant manufacturing capability to Monclova, Mexico - near Trinity and other railroad supply companies. For Greenbrier whose margins are significantly inferior to its larger competitor, this is a positive, as it allows for operational expertise to more freely mingle.

With demand almost irreversibly strong, line of sight to stable recurring cash flows, potential margin expansion in the manufacturing business, and European operations closer to being back on their feet, the missing piece is actual execution. This hasn’t yet occurred. Typically, when a company is in an opportunity rich position, as Greenbrier’s is, an able management team begins to manifest positive developments for the company and therefore the stock, before or while the operational outcomes are occuring. The Company has to execute, and should it, the stock should prove to exceed White Brook’s hurdle for continued investment. If execution continues to falter, while I imagine it would be a ripe candidate for activism, White Brook’s investment will be rethought.

The Baron Health Care Fund initiated positions in 3 companies this quarter, Cigna (CI), HCA Healthcare (HCA), and Option Care Health (OPCH). They briefly outline their theses below.

We initiated a position in Cigna Corporation, a health services organization with two primary segments, Cigna Healthcare and Evernorth. Cigna Healthcare provides health insurance products, including a business in which Cigna provides administrative services only to plan sponsors (employers, unions, and other groups). Evernorth provides a portfolio of health care services, including pharmacy benefit management (PBM) services, care delivery services, data and analytics solutions, and distribution of specialty drugs. Each segment has a portion of business that provides steady, predictable growth. These foundational businesses, which account for roughly 60% of total revenue, include the U.S. commercial business, the PBM business, and international. The other 40% of revenue comes from higher-growth businesses, including the specialty pharmacy business, care delivery services, and Medicare Advantage. Management targets 10% to 13% annual EPS growth over the long term. The stock trades at a significant discount to industry peers because of the company’s commercial health insurance and PBM business mix. We think the PBM business will benefit from the biosimilar wave in the next few years, and as Cigna’s higher growth businesses become a bigger percentage of the overall mix, we think the stock can appreciate at least in line with its annual EPS growth with potential for valuation expansion.

We initiated a position in HCA Healthcare, Inc., one of the nation’s leading providers of health care services. As of September 30, 2022, HCA owned, managed, or operated 182 hospitals and approximately 2,400 ambulatory sites of care in 20 states and the U.K. We think long-term demographic trends as well as HCA’s strong presence in attractive growth markets where there is net population migration position the company well to generate sustainable long-term growth. Prior to the COVID pandemic, management targeted long-term top-line organic growth of 4% to 6% with pricing/mix running in the 2% to 3% range and adjusted patient admissions increasing 2% to 3%. Although COVID has been disruptive to this framework, management believes organic revenue growth can return to its targeted 4% to 6% range with positive margin leverage possible at the high end of the range. Recently, the company has seen contract labor costs and wage pressure start to moderate and volume trends are improving. HCA also has a long-term track record returning capital to shareholders through special dividends and share repurchases.

We initiated a position in Option Care Health, Inc., the largest independent player in the $15 billion U.S. home and alternate site infusion market. We believe Option Care is well positioned to capitalize on the ongoing shift to lower-cost sites of care and the proliferation of new specialty drug treatments. Home infusions cost 40% to 70% less than infusions at a hospital. Option Care’s footprint, with over 150 locations, allows it to serve roughly 96% of the U.S. population in a market growing 5% to 7% a year. The company has a well-diversified portfolio of therapies and provider relationships with no customer concentration, enjoys in-network status with all larger payors, and has low direct government reimbursement risk as Medicare currently does not cover home infusion. We estimate the market would double if this were to occur in the future. Given its geographic coverage and therapeutic expertise, the company is assured a seat at the table to discuss new innovative episodic or fully capitated models with payors. It also has strong relationships with relevant drug manufacturers, facilitating early access to newly approved drugs and preferred supply arrangements, while its size and scale provide purchasing power. Management believes the company can continue to generate high singledigit organic revenue growth and mid-teens EBITDA growth. There is also an opportunity to enhance growth through M&A. The company has an excellent track record of acquiring and integrating acquisitions and, with 45% of its market still made up of regional and local providers, there is a meaningful consolidation opportunity.

Until next time! - EP