Welcome back to Elevator Pitches!

We will save you time by curating the best stock ideas from the investment letters we read each quarter.

If you find what we do helpful in your process, please forward to a friend or colleague.

Subscribe below so you don’t miss future issues.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter if you’d like to be included in a future issue.

A few late-arriving investment letters have hit in the last week, and we’re happy to share 3 more new ideas.

Let’s get to it.

As outlined in their recent investor letter, Greenhaven Road Capital is currently in the midst of its worst drawdown since inception. That hasn’t stopped them from looking for new ideas. Did they find a winner in Hagerty, Inc. (HGTY), a specialty insurance company focused on premium and classic cars?

NEW INVESTMENT – HAGERTY (HGTY)

A SPAC trading at over 200X forward earnings run by a man who almost became a priest should be either the set-up to a bad joke or a pitch for a short investment. However, out of the rubble of SPAC-ageddon emerges a very interesting company: Hagerty, Inc. (HGTY).

Earlier this month, we held an Annual Meeting for LPs that included a “Fireside Chat” with Hagerty’s CEO. The interview is worth watching as it covers much of the ground of this write-up and provides additional details. (LINK)

Hagerty stood out to us when they disclosed their historical and prospective investors during their “de-SPAC” process. State Farm, the largest auto insurance company in the U.S., invested $500M in the SPAC deal at $10 per share, and specialty insurance company Markel not only owned 25% of Hagerty prior to the de-SPAC, but also invested an additional $30M in the deal at $10 per share. Two sophisticated insurance companies investing in another insurance company… It was unlikely the trailing P/E ratio that convinced State Farm to part with half a billion dollars and have their CEO join Hagerty’s Board, so we decided to do some digging.

Today, 92% of Hagerty’s revenues are insurance-related. I will describe the other pieces of the business shortly, but the economic engine that powers the company is automobile insurance. More specifically, the company specializes in a particularly niche insurance category: classic and collectible cars. Hagerty insures everything from 100-year-old cars requiring a crank to start to Mazda Miatas from the 1980s and modern “Super Cars” (McLarens, Bugattis, Lamborghinis, etc.) that are currently in production. What differentiates a Hagerty policy from the traditional policy you have on your Ford / Toyota / etc.? Hagerty policies aren’t for “daily drivers.” Instead, they are insuring people’s prized possessions like the old convertible that the owner only drives on sunny Sundays to a farmers’ market. People treat their “toys” well, and this shows up in Hagerty’s numbers with their loss ratio (amount paid out for claims) coming in around 41% vs. 70%+ for a typical auto insurer.

In capitalism, profit pools typically get competed away, but Hagerty has not seen this happen to date despite being in existence since the mid-80s. The low loss ratio is not a new phenomenon – it has consistently been nearly half the industry average. Can that persist going forward?

Pricing and servicing a policy for a collector car has its pitfalls. To cite one of the company’s simple examples, take the Chevrolet Camaro from 1969, considered the finest year for classic Camaros. Over 240k Camaros were produced in 1969; however, they were made in 147 different variants. The least valuable version is worth approximately $11,000 while the most valuable version is worth over $1M. An insurance underwriter better understand which version they are insuring. In addition, unlike most automobiles, the value of classic/collector cars tends to appreciate each year. Both the insurance company and the customer need to understand the rate of appreciation for the model in order to avoid a situation where the insurance proceeds are insufficient to replace a beloved car. Classic cars also face service challenges. If one needs to replace the windshield on a 1915 Model T Ford, trying to file (let alone complete) a claim with the 800-number of a mega insurer will likely be a frustrating experience. Hagerty has a whole team dedicated to helping its members source specialty parts, a service of extremely high value to customers. Large insurers are not equipped to service this niche market well – they have neither the data nor the operational support for this niche product that ultimately equates to a small percentage of their overall insurance book.

The typical owner of classic/collector cars loves their cars but also has many other items needing insurance (homes, boats, daily drivers, etc.). Consequently, nine of the top ten insurers (not Geico) partner with Hagerty to price and service insurance to their policyholders with classic and collectible cars. Why would they partner with a company some would see as a competitor? Hagerty provides more accurate pricing and better service and reduces the likelihood of losing excellent customers by mishandling a classic/collector car policy that is only a small, but emotionally charged portion of the overall relationship. By not offering homeowners, umbrella, and other insurance products, Hagerty avoids channel conflict, meaning that those that would otherwise be Hagerty’s competitors are instead their partners, creating a favorable competitive dynamic within the industry that provides at least a partial explanation for the persistence of the company’s low loss ratio.

For more than a decade, Hagerty has grown at three times the rate of the overall auto insurance industry, fueled by high retention rates (90%+), effective marketing (more on that later), and the partnerships described above. What is not obvious when first studying the company is that existing partnerships tend to be a source of ongoing growth. Many auto insurance agents are independent, meaning, for example, that they may represent Allstate as well as other companies. Hagerty has a partnership with Allstate, but agents do not have to use Hagerty or switch their customers off an inferior Allstate classic car policy on to an Allstate/Hagerty policy. That means that the book of business on classic cars not with Hagerty has continued to grow at the same time as the mutual policies have. This semi-captive audience is a source of value because Hagerty has a “hunting license” within that population and slowly converts over agents and policies. The fact that nine of the top ten insurance companies are partners does not mean that future growth is stunted – Hagerty is still early in the penetration of those customer bases.

The market size for classic and collectible cars is larger than I would have thought. Hagerty estimates that there are over 43M registered classic and collectible cars. That number grows each year as new collector cars (McClaren, Ferrari, etc.) are produced and other cars “age into” the category (25 years old or more). Hagerty currently has ~2M cars insured, so there is a long runway for growth.

In addition to acquiring customers through the partnership model, Hagerty also acquires customers directly. Unlike many large insurers that blanket the NFL television broadcasts with commercials every fifteen minutes, Hagerty focuses on content and events that tap into classic car lovers’ passion for cars. They now own several of the largest classic car shows in the United States in addition to the second-largest (by circulation) automobile magazine, a YouTube channel focused on classic cars with over 2M subscribers, and an automobile valuation tool that is widely used. Hagerty also operates a “Drivers Club,” which provides roadside assistance and weekly emails to over 2M members. This diverse set of assets is intended to fuel peoples’ passion for cars – insurance is rarely, if ever mentioned directly. However, these offerings serve as very effective customer acquisition tools. By our math, Hagerty’s customer acquisition costs are less than half the industry average.

To further monetize their core insurance business more effectively, Hagerty entered the reinsurance business in 2017-18 with the creation of HagertyRe. Since its acquisition of Essentia in 2013, Markel was Hagerty’s captive reinsurance partner whose primary function was to provide their balance sheet and credit rating to support the underlying growth of Hagerty’s insurance book. The reinsurance business is very attractive for both Hagerty and Markel due to the low loss ratios experienced in the underlying book of business. To illustrate this point, let’s see how $100 of premium flows through the reinsurance business. First, Hagerty gets to keep ~$42 as a commission for servicing the policy. $32 of that is a base commission and $10 is a contingent commission that is earned if loss ratios stay within a pre-determined range. The next ~$41 will be paid out to policyholders because of accidents incurred. (We are now up to ~$83 out of the $100 premium.) Next, ~$6 will used on operating expenses and reinsurance costs. The net result is that, for every $100 in premium received, HagertyRe earns ~$11 in operating profit. That sounds great by itself, but there is more: for every dollar retained in HagertyRe’s business, it can write $3-4 in premiums. In other words, the return on every incremental dollar retained in the reinsurance business is 30-40%.

For the past two decades, Hagerty has been led by CEO McKeel Hagerty. His parents started the company in their Michigan home in the 1980s, initially focusing on insuring wooden boats on the Great Lakes. Recognizing that people love their toys and, if done properly, insuring the toys was a good business, they added collector cars and began to expand beyond Michigan. On paper, their son is not a person you would select for the job. On paper, he is a tenth-round draft choice. He was an English and Philosophy major in college and then then decided to enter seminary, studying to be a Russian Orthodox priest and pursuing higher education. However, since it came under the leadership of McKeel and his sister Kim (who held various roles before retiring in 2014), Hagerty has grown the company from 30 employees to over 1,700 today while launching the partnership model, entering the media business, beginning the Driver’s Club, creating their specialty valuation tool, and buying up classic car shows. McKeel has a very folksy demeanor, but this is no simple small-town boy. In 2016, he was elected to serve as the global chairman for YPO (Young Presidents Organization, the world’s largest CEO organization) and has traveled the world interacting with business leaders. The company has a strong culture and has been voted among Fortune’s Best Places to Work for the past four years. If one peels back the layers, this business has been assembled methodically and is about to enter its next phase of growth.

Insuring cars with low loss ratios, low customer acquisition costs, and low churn is an excellent business. Creating and supporting a marketplace for classic and collectible cars might be an even better business. For a marketplace business, there are three important components – the supply side (goods), the demand side (customers), and a trusted intermediary. Hagerty has these pieces. They can feed the demand side through their media properties and leverage email relationships with over 2M Hagerty Drivers Club members. They also have a top-of-funnel position controlling the valuation tool that is used across the industry. On the supply side, Hagerty owns the software used by over 200 leading classic car dealers to manage their inventory and also owns several car shows that have traditionally hosted in-person auctions as part of their programming. Through their recent acquisition of Broad Arrow Group, Hagerty also acquired the management team that led the automobile auction and financing business at Sotheby’s. As an insurance company and the name behind the valuation tool most widely used in the classic car space, Hagerty is starting from a position of trust.

While Hagerty has been laying the groundwork to enter the auction business for several years, they only completed their acquisition of Broad Arrow Group last quarter and have since held two auctions selling a total of $70M+ of classic cars. They also began to offer classified ads, but the real volume will come over time, as an alternative to Bring-A-Trailer (a popular auction platform for classic and enthusiast vehicles) was recently announced and will debut next month. The company’s data suggests that, of the cars that Hagerty insures, $12B in market value traded hands in a combination of auctions and private transactions over the last 12 months. In addition to monetizing a passionate car-loving community that Hagerty has assembled, the marketplace provides an opportunity to both improve retention and acquire new customers since the moment of purchase is an ideal time to attach a new insurance policy. Given that a Hagerty member selling their single classic/collector vehicle is the largest cause of churn, Hagerty is simply better positioned to monetize and execute such transactions than traditional auction houses or marketplaces.

Short-term financing is yet another ancillary business that will emerge from the marketplace business. Hagerty, which has the industry leading valuation tool, insurance relationships with millions of owners, and a strong balance sheet, is in prime position to provide short-term loans to facilitate transactions (typically at 50% loan to value). Frequently, these loans are essentially bridge financing until a collector can sell another car, a transaction which Hagerty again is well-positioned to capture vs. competitors. The flywheel at Hagerty is spinning – what would once have been a simple car insurance policy can now turn into a buyer’s commission, a seller’s commission, listing fees, and financing fees.

While the marketplace business has the potential to be quite large, it is in its infancy and will likely not be a source of large profits in 2023 or 2024 as Hagerty invests in growing the business. Fortunately, Hagerty has two contractual events that will occur in 2023. The first is that State Farm will onboard 470,000+ policies to Hagerty. This is part of their 10-year contractual relationship and $500M PIPE investment. The State Farm opportunity has not contributed any revenue for the past two years, instead actually only contributing costs as massive systems integrations and upgrades have been undertaken. Those costs are now dropping off as the partnership becomes revenue-generating next year. The second contractual event will be the change in reinsurance revenue share between Markel and Hagerty, increasing Hagerty’s share of revenue from 70% up to 80%.

One would think that the upcoming contractual events and burgeoning marketplace opportunity would be well understood and reflected in the HGTY share price, but to us that seems to not be the case. One more casual indication of investor apathy is that, on the website SeekingAlpha, fewer than 500 people “follow” Hagerty vs. more than 42 million for Apple and hundreds of thousands for many companies you know. It was a SPAC, screens expensive (in part because State Farm has been all expense no revenue), and has a small free float (less than $3M trades daily). Until last week, Hagerty had only one sell side analyst who, in their initiation report, did not even give financial projections beyond 2022 for 2023. Last week, a new analyst initiated coverage and did include 2023 projections, but these somehow appear to ignore the State Farm policies and the marketplace revenue, which are both 2023 events.

Hagerty has grown at 3X the overall insurance industry and, with increased penetration of their partnerships, the realization of contractual events, and launching of the marketplace, I believe the topline growth rate will inflect to over 30% per year for the next few years. Loss ratios should hold steady at ~40% lower than the industry average, and customer acquisition costs will likely decline further to less than half that of the industry average. Because of the statutory nature of the product (you need insurance if you want to drive your car), the contractual events in 2023 (State Farm and Markel/reinsurance), and a growing marketplace, Hagerty is well-positioned to withstand a recession should one occur in 2023.

Hagerty will continue to screen expensive on an earnings basis for the next few years as they invest in their marketplace and international insurance businesses. However, at the core of Hagerty is a very profitable car insurance business with excellent unit economics and a very long runway for growth as they continue developing the ecosystem to support, sustain, and monetize peoples’ passion for cars.

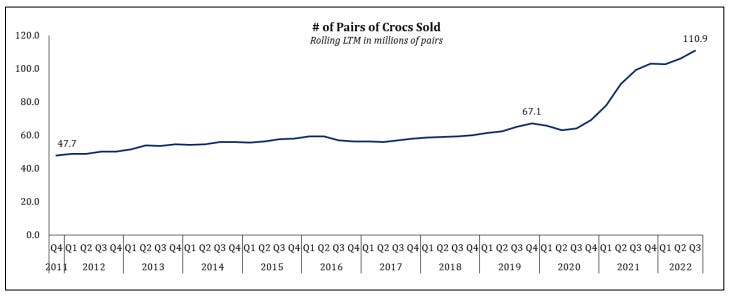

Voss Capital initiated a new position in the shoe company, Crox Inc. (CROX). As a young-ish dad living in the suburbs, am I required to disclose that I own two pairs?

Crox Inc. (CROX)

Crox is a new long position. While the shoes are often perceived as a fad, it might surprise many of you that the Crox brand has not only endured for 20 years but is still growing by >20% organically (on top of 73% revenue growth in Q3 last year) with mid-to-high 20% operating margins.

Aside from being a consumer discretionary company and perceived Covid lockdown beneficiary at peak earnings, why did the market offer up the opportunity recently to buy CROX at its lowest earnings multiple ever? The company levered up to buy a relatively unknown shoe brand HEYDUDE for $2.5 billion in an auction process that was at first looked at with great skepticism. With the passage of time (and initial results), we think the market is coming around to the idea that the acquisition was a good one as the shoes will grow to become even more wildly popular. Academy Sports (ASO) recently called them out on their September 7th earnings call, saying, “We're also excited to launch HEYDUDE in all stores in July just in time for back-to-school. We're seeing strong early results and expect HEYDUDE to be a sales driver versus the remainder of the year."

HEYDUDE has already greatly surpassed CROX management team’s initial growth expectations, to such a degree that it turns out they only paid an estimated ~9.5x NTM EBIT (a sizeable discount to CROX’s historical median ratio of 12.0x), for a high margin, rapidly growing brand. As a relatively unknown and underpenetrated shoe brand, we gained conviction that the company can follow its Crox growth playbook and systematically increase HEYDUDE’s distribution both domestically and internationally to drive a 20% revenue CAGR over the next few years. Since 2014, the CEO has had an impeccable track record of delivering on targets laid out and we think the company can continue this trend of excellent execution with HEYDUDE.

In sum, our view is that we bought CROX at half its historical median valuation while the company is guiding for a revenue growth rate of nearly double its historical rate with over triple its historical operating margins. Our Base Case price target is $160 (70% upside within the next ~2 years), which would be 10x our discounted 2025 EBIT estimate—still a 17% discount to its historical median of 12x.

Headwaters Capital bought a new position in UFP Technologies (UFPT), a small cap supplier to the medical devices industry.

UFP Technologies: Materials Expertise & Specialized Manufacturing Creates a Valuable Partner to the Med Device Industry

Summary Thesis

High single digit organic revenue growth underpinned by a growing medical end market, accelerating new product wins from increased R&D and improving customer retention. Organic growth supplemented with strategic M&A.

Highly visible revenue growth supported by medically necessary consumable products and long duration contracts with high switching costs.

Margin expansion as portfolio repositioning is largely complete and COVID supply chain disruptions subside.

Management team with a proven history of execution combined with insider ownership provides confidence that the company will continue to be good stewards of capital.

Company Overview

UFP Technologies engages in the design, development and manufacturing of custom-engineered components, devices and packaging primarily in the medical end market. Leveraging its access to and engineering expertise in specialty foams, plastics and composites, the company designs and manufactures parts and devices that are single use in nature. Representative products include surgical robotic drapes, vascular tools, wound therapy products and orthopedic devices.

In many ways, UFP serves as an outsourced R&D partner for clients by assisting during front-end product design and engineering. Through the development of customized machinery, manufacturing expertise and a network of FDA certified manufacturing facilties and clean rooms, UFP can oversee the transition from prototype to commercial production. The highly engineered nature of UFP’s products and the rigorous FDA approval process for both new product introductions and manufacturing techniques leads to deep and long-lasting customer relationships for the company. UFP counts 26 of the top 30 medical device companies as customers, which highlights the company’s design, engineering and manufacturing expertise in the medical market.

UFP's revenues are highly visible as the medical end market has relatively stable demand given the critical nature of the products and most of UFP's end products are consumable in nature in the form of single-use or single patient devices. Long-term contracts with high switching costs provide even greater revenue visibility for the company. The steady nature of UFP's revenue allows the company to invest confidently in both R&D and capacity expansions that generate high returns on capital. As the company continues to focus more on product development alongside customers, it not only builds stronger customer relationships, but it will also result in higher margin revenue as these more innovative products come to market.

Business Transformation

UFP has completed a significant transformation from a commoditized packaging company serving cyclical end markets to a custom manufacturer of specially engineered components and devices for the highly regulated medical end market. In 2015, 41% of UFP's revenue was generated from the medical end market and the majority of UFP's other revenue came from commoditized packaging to cyclical end markets such as consumer, industrial and electronics. Today, 80% of UFP's revenue is generated from the medical market, which is the result of a multiyear strategic plan to exit commoditized, low margin packaging businesses and instead focus on highly engineered medical components and devices that carry higher margins. The regulated nature of the medical end market creates high switching costs for UFP's customers given the time and effort required to reach FDA approval. The high switching costs combined with long product life cycles provides UFP with an annuity-like revenue stream once a contract is won. A brief timeline of the key events in UFP's transformation is shown below.

Creating the Platform to Grow (2013-2016): UFP undertook a multi-year strategic repositioning of the portfolio to better position the company for future growth in the medical end market. The process involved facility consolidations, investments in new production capabilities, capacity expansions and an ERP system upgrade. During this period, the company was forced to requalify programs with existing customers, incurred restructuring charges and saw margin degradation as facilities were initially underutilized. However, this comprehensive portfolio overhaul created a platform that could better serve the medical end market.

Investing in Medical Growth (2018): Acquisition of Dielectrics, which brought specialized manufacturing capabilities to UFP and deeper penetration into the medical device end markets. Following the acquisition of Dielectrics, medical sales accounted for 60% of revenue compared to 47% in the year prior to the transaction.

Medical Market Expansion (2021): UFP completed 3 acquisitions in the medical end market in late 2021 and early 2022. The acquisitions enhanced manufacturing capabilities, added new customers and increased the company’s offshore manufacturing footprint. Historically, as products reach maturity, med device companies have sought to move manufacturing offshore to reduce costs. UFP's customers encouraged UFP to expand their offshore manufacturing capabilities as they wanted UFP to retain the business given that the FDA had already certified UFP as the manufacturer. Prior to the offshore manufacturing capabilities, UFP lost this business, which resulted in annual churn that UFP had to offset through new contract wins. In addition to acquisitions, UFP also built its own manufacturing facility in Mexico, which is set to come online in 2H ’22. The expansion of the company’s offshore manufacturing expertise should allow the company to retain more programs as they reach maturity, which will reduce customer/product churn. Pro forma for these acquisitions and the divestiture below, medical sales now comprise 80% of UFP revenue.

Portfolio Pruning (2022): At the beginning of Q3 ’22, UFP divested its low margin Molded Fiber packaging business. Proceeds were used to pay down debt associated with the three acquisitions above. Pro forma for the acquisitions and divestiture, leverage is <1.0x on a net debt/EBITDA basis.

This historical background illustrates that UFP is led by a management team with a long-term focus and a proven history of successful acquisitions and divestitures. Acquisitions that add manufacturing capabilities, materials expertise or geographic expansion all serve to make UFP a more valuable partner to its customers and, given the strong cash flow of the business, I expect M&A to continue. The successful transformation of UFP into a preferred R&D and manufacturing partner for the medical device industry gives me confidence that this management team is well suited to continue programmatic M&A. Insider ownership by the CEO (6% of the Company’s stock worth $40mm) aligns management with shareholders and provides further comfort that management will be good stewards of capital.

UFP still derives 20% of its revenue from the auto, aerospace and defense and industrial end markets. A&D has many of the same characteristics as the medical end market in the form of long duration contracts and highly engineered products. The industrial and auto markets are more commoditized and could be sold or exited in the future (similar to the recent sale of the molded fiber business), although the company continues to benefit from product innovations in these end markets that can also serve the medical market.

Financials

As described above, UFP's transformation has been a long process, but is largely complete today. The culmination of the transformation into a medical device supplier with higher organic growth and margins has been masked by COVID disruptions which have impacted both top line and profitability. Consolidated organic growth for UFP averaged 2.6% from 2015-2019 but is likely to sustain at a significantly higher level now that the portfolio repositioning is largely complete. While the company targets organic revenue growth on a consolidated basis of 57%, I believe the company will grow faster than this target given that the medical end market for UFP has grown at a +6% organic CAGR since 2015 (+9% excluding COVID impacted 2020). Additionally, UFP’s medical end market growth is likely to accelerate as broader offshore capabilities reduce churn while an increased focus on product R&D should lead to more new product wins. The accelerating organic growth will be supplemented with a steady M&A program, resulting in top-line growth of 10-15%, depending on the pace of acquisitions.

From a margin perspective, UFP expects improvement in gross margins as supply chain pressures ease and manufacturing utilization increases. Management currently expects operating margins to improve from ~11% (LTM Q2 '22) to 12-15%, supporting operating income growth well above revenue growth. As CAPEX normalizes following the recent capacity expansions, FCF should compound at a 15-20% CAGR for the next 5 years. The strong free cash flow and low leverage (<1.0x net debt/EBTIDA) provide the company with ample capacity for strategic M&A.

At a minimum, UFP should maintain its valuation multiple of 14x EBITDA. However, as the portfolio repositioning becomes more visible in 2023, growth rates accelerate and margins improve, the company could command a valuation premium in line with other specialty manufacturers in the 16-18x EBITDA range.

Investment Summary

UFP is a perfect example of the type of business that can tax efficiently compound for many years and is ideally suited for the HCM portfolio. UFP's competitive advantages in the design and manufacturing of medical devices and components supports a platform that can execute on the long-term growth opportunities in this market. Recurring revenue from a growing medical end market combined with long-term customer contracts provides high visibility into future revenue growth. Improving margins will generate healthy free cash flow that can be deployed into strategic M&A that serves to deepen UFP’s value proposition to customers. An experienced management team with high insider ownership provides confidence that management will be disciplined allocators of capital.

The combination of all these factors supports an expectation that UFP can compound investor capital at a 15%+ CAGR over the next 5 years. Growing investor appreciation for the transformed UFP portfolio presents an opportunity for even higher share price gains as the market begins to appreciate the durability of UFP's revenue and the improved return profile of this primarily medical portfolio.

Until next time! - EP