EP132: Wire to Wire

Stock Ideas From Investment Professionals

Welcome, subscribers!

We’ve reviewed another interesting batch of investor letters and are excited to deliver more actionable ideas in this week’s issue. This week’s collection spans a variety of industries, each with a common thread: investors looking for durable assets where complexity, cyclicality, or near-term uncertainty may be obscuring long-term value.

If you know someone who enjoys investor letters and discovering new ideas, feel free to forward. 📬

This week, our five new ideas include:

A utility sum-of-the-parts story hiding in plain sight.

A mission-critical lab tools company with high switching costs.

A water and hygiene compounder with durable regulatory tailwinds.

A power infrastructure play on AI-driven electricity demand.

A serial acquirer targeting a large and highly fragmented market.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

Voss Capital’s pitch for Sempra is our highlighted idea this week. The setup is a classic sum-of-the-parts story hiding in plain sight: a California utility wrapper is masking the value of Oncor, Sempra’s high-growth Texas transmission and distribution asset. Voss believes Sempra can unlock that value through simplification, asset sales, and a potential tax-free spin of Oncor, creating a path to meaningful upside by 2028.

New Core Long: Sempra Energy (SRE)

Voss has accumulated a significant position in Sempra Energy (NYSE: SRE). SRE is a utilities conglomerate that we believe has the opportunity to unlock significant value through simplification. Sempra’s current public structure, dominated by two California utilities that contribute more than half of earnings, masks the rapidly compounding intrinsic value of the fastest growing and largest transmission & distribution (T&D) utility in North America: Oncor Electric in Texas.

SRE trades at a 17.8x NTM P/E multiple, which is in-line with lower-growth regulated peers. This consolidated valuation fails to account for the dramatically divergent paths of Sempra’s assets.

Oncor: A pure-play regulated wire network operating under a highly constructive Texas regulatory environment, entirely insulated from California politics and wildfire liabilities. Oncor is experiencing unprecedented secular tailwinds from Permian Basin electrification, population growth in D/FW and across central Texas, and a significant upgrade to the state’s transmission infrastructure.

California Utilities, San Diego Electric & Gas (SDG&E) and Southern California Gas (SoCal Gas): SDG&E provides electric services to 3.6 million people and natural gas services to 3.3 million people who live in San Diego County and Orange County. SoCalGas is a pure natural gas utility providing services to over 21.3 million people in Southern California, namely around the LA area. SoCal has over 3,000 miles of transmission pipelines, bringing large amounts of natural gas to the region and over 52,000 miles of distribution lines that bring the gas directly to homes and businesses in the area. It is the largest “last mile” natural gas distribution utility in the country (a/k/a a Local Distribution Company, LDC).

Sempra Infrastructure: Sempra Infra operates an extensive network of pipelines and clean energy projects across the U.S. and Mexico, and major liquefied natural gas (LNG) export terminals on both the Gulf and Pacific coasts in various stages of development. The Sempra Infrastructure segment is a highly valuable, yet complex collection of assets in terms of accounting, diversity and development stage – complicating the picture amongst an otherwise comparable utilities universe.

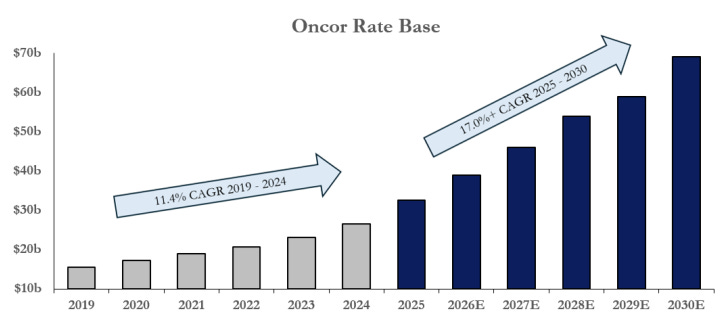

It is said Mother Nature quipped “you can’t squeeze all the weather in the world into one week.” Texas replied, “hold my beer and watch this.” Well for the next several years, Oncor has blustery west Texas gusts at its back. To put some numbers around this, Oncor currently has about $31.5 billion of Rate Base. Rate Base is essentially the amount of (depreciated) invested capital that has been put in place for which a utility is legally allowed to earn a regulated rate of return on. Over the next five years alone, the company has plans to spend a staggering $47.5 billion of capital, which translates into its Rate Base growing to $69 billion by year end 2030. Oncor has highlighted an additional $10 billion on top of that which they are optimistic will be put to work during that time frame but have yet to include in the base plan. In other words, there is upside to what will be a nation leading 17% annual Rate Base growth in the current plan. Maybe everything really is bigger in Texas.

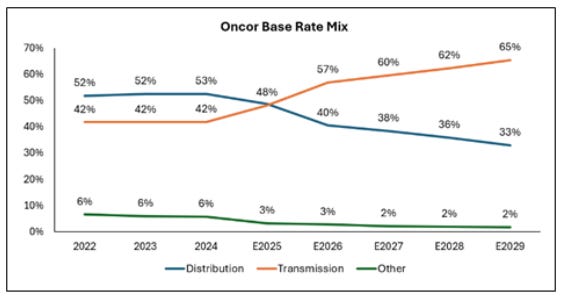

A disproportionately large part of this capital plan is related to transmission projects that have already been approved. The visibility on these projects is high, and we do not believe there is a significant risk of project cancellations. These capital plans are NOT dependent on large Data Center build outs or electricity demand. It is also important to note that transmission-related utility assets (power lines moving bulk high-voltage electricity over long distances) are regarded as the highest quality assets in the industry. Over 70% of Oncor’s 5- year base capital plan is expected to be spent on transmission related projects, growing at an eye-popping ~22% CAGR. This is much faster than six of the seven ‘Mag-7’ stocks, only slightly trailing NVDA’s growth expectations—but without all the cyclicality and uncertainty over LLM demand or dependency on circular financing for its own customers.

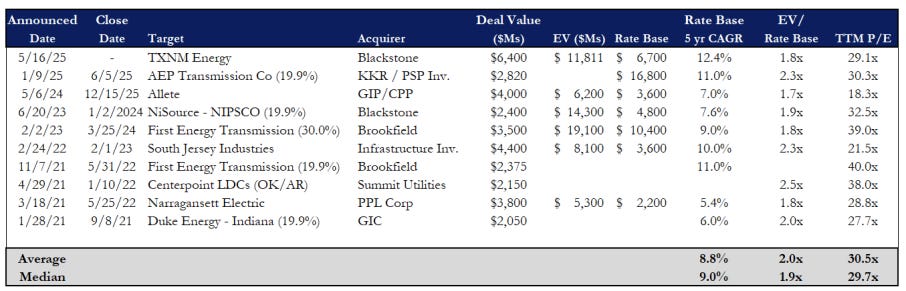

There have been several recent transactions in the industry for minority stakes of Transmission & Distribution companies completed at very attractive multiples. Infrastructure-focused private equity buyers have shown broad appetite for regulated utility assets, attracted by rate base growth and earnings stability, with one comparable transaction reaching 40.0x earnings. None of these companies below had or have near the growth rate that Oncor expects to see over the next five years.

The dynamics of the West Coast utilities are notably different. There are three major publicly traded California Gas & Electric Utilities – Pacific Gas & Electric (PCG), Edison International (EIX) and Sempra (SRE) - with PCG and EIX being “pure play” California utilities. In California, growth rates are below industry average as there is lower population growth and lower commercial & industrial demand growth in the region. Rate Base at SRE (SDG&E / SoCal), EIX, and PCG are expected to grow 5%/7%/9% respectively over the 2025-2030 timeframe.

Wildfires have been the defining topic for utilities in California over the last decade. The destructive Camp Fire in 2018 created massive legal liabilities and in turn led to the bankruptcy of PCG. This led to incremental wildfire regulation reform in the state including the passing of AB 1054 which created a wildfire fund meant to cover future costs associated with wildfires, and PCG exited bankruptcy in 2020. Over the subsequent years, EIX and PCG valuations recovered such that they were trading around 16x/14x NTM P/E in December 2024. In January 2025 another catastrophic wildfire ignited, and fresh fire fears flared. The uncertainty depressed valuations into the high single digits by summer of 2025 before they stabilized again. SRE was more insulated from the brunt of the wildfire de-rating but was still affected.

Sempra’s California utilities have substantially lower wildfire risk than EIX and PCG because 1) SoCal gas is a natural gas transmission and distribution company, and as such is not at risk of igniting a fire and 2) San Diego Gas & Electric was at the forefront of wildfire mitigation plans many years before peers and has over 60% of the electric distribution system undergrounded (a buried electric line does not have risk of starting a fire, while an above ground line does). SDG&E has not been involved in a catastrophic wildfire in nearly two decades. Given its superior asset profile, if Sempra’s standalone California utilities traded publicly, we would expect it to trade at a meaningful premium to EIX/PCG.

There has continued to be favorable reform on California Wildfire Policy. In September 2025 SB 254 passed which extended the California Wildfire Fund that was originally created in 2019. Contribution requirements for the fund were favorably split 50/50 between utilities and ratepayers. It strengthened liability caps (20% of equity rate base) and instructed the California Earthquake Authority to issue a comprehensive report and include further recommendations of reforms, which they did in April. The report highlighted that 1) wildfire risk is really a “whole of society” problem and not just a utility problem, 2) the current legislative framework was created as a temporary measure until more durable legislation was formed, and 3) there is significant cost of legislative inaction. The reforms over the past few years are moving away from a stance that was highly punitive to the California investor-owned utilities. We believe that over time, there will be a more equitable solution to absorbing wildfire losses in the state. It is not in the best interest of Californians to put most of the burden of wildfire losses on the investor-owned utilities in the state as this creates weaker utilities with a higher cost of capital, which in turn leads to higher utility rates for Californians.

A Potential Texas Sized Alpha Unlock Opportunity

Sempra can execute a tax-free spin-off of its 80.3% economic interest in Oncor to Sempra shareholders. The newly formed "SpinCo" would establish the premier, pure-play, and highest-growth public transmission utility. Unburdened by California wildfire headlines, we think Texas T&D pure play Oncor will attract low-cost infrastructure and ESG-focused capital, prompting an immediate market re-rating and likely garnering the highest multiple in public utilities. Concurrently, the remaining California business ("RemainCo") would serve as a high dividend, stable utility vehicle attractive to value investors constructive on West Coast legislative updates with a clear opportunity to re-rate as fire risks fades into the rearview. With more constructive regulation, these utilities will also be more apt to put capital to work in the state and thus improve rate base and earnings growth.

Sempra Infrastructure owns a bundle of energy related assets, in various stages of operation – some being contemplated, some being constructed, and others in operation. Sempra has already entered an agreement to sell a 45% stake in Sempra Infrastructure Partners (SIP) to KKR and CPP Investment Board for $10.0 billion cash, implying a robust valuation of 13.8x EBITDA and a total equity valuation of $22.2 billion ($31.7 billion EV). Sempra can aggressively utilize these structural cash inflows—arriving in three scheduled tranches ($4.7 billion in Q3 2026, $4.1 billion in Q4 2027, and $1.2 billion in 2033) —to de-lever the parent balance sheet and self-fund the enormous capital expansion requirements at Oncor without the need to issue a single share of equity.

The complicated accounting and disparate assets within the Sempra Infrastructure segment unnecessarily complicates the story at Sempra (now accounted for as a “held for sale” asset). After the completion of the sale, Sempra will own ~25% of Sempra Infrastructure Partners. When the remaining stake of Sempra Infrastructure Partners is sold, Sempra and Oncor can trade as pure play utilities. Sempra is eligible to sell its remaining stake as early as January 2029, lining up with a late 2028 corporate restructuring.

At the end of 2028, assuming a 30x Forward Price/Earnings multiple for Oncor (slight premium to other growthy utilities given its Transmission dominance and even faster growth rate), the equity would be worth $78 billion, and Sempra’s ownership at 80.25% would be worth $62.5 billion. This would imply a valuation of 1.9x Enterprise Value / Rate Base, a steep discount to several recent transaction comps in much slower growing peers that were in less favorable regulatory jurisdictions. Assuming the California utilities trade for 16.0x earnings, where the California pure plays more prone to fire risks were valued at just 18 months ago, that is another $26 billion of value. The combined value would be $141/share, +53% from the current share price and offering a 17% IRR between now and the end of 2028. Of note, SRE shares trade ~$375 million of volume per day, thus despite a 9% portfolio weight across the Voss complex, our stake remains only one half of one day’s trading volume.

Paid subscribers can keep reading for four additional ideas, including a precision instruments leader with mission-critical products and high switching costs, a water and hygiene compounder with durable regulatory tailwinds, a power infrastructure beneficiary of rising electricity demand, and a serial acquirer pursuing a large-scale consolidation opportunity in a fragmented market.

If you find value in seeing how professional investors frame new ideas, upgrade to keep reading and get the full archive.

Need a nudge? Many subscribers work in asset management, research, or corporate finance and expense it as a research tool. Here’s a quick script you can use.

Hi [Manager’s Name],

I’d like to expense a subscription to Elevator Pitches, a newsletter that curates stock ideas from professional investor letters, often highlighting overlooked opportunities and special situations.

With a paid subscription, I’d receive full access to every stock write-up they publish each week, which would support my ongoing market research and idea generation.

The cost is $90 for the full year. Given the depth and frequency of the analysis, I think it’s a cost-effective addition to my research toolkit.

Please let me know if this works.

Best,

[Your Name]