EP123: Under Pressure, Underpriced

Stock Ideas From Investment Professionals

Welcome, subscribers!

Our latest issue brings together more fresh pitches from professional investors across a variety of industries. Each highlights a familiar pattern we like to study: short-term pressure, overlooked durability, and valuation gaps that still look wide.

Know someone who enjoys thoughtful stock ideas? Please consider forwarding. 📬

This week, we highlight 6 new ideas, including:

Full-stack payments platform: execution strong despite the recent selloff.

Specialty chemicals cyclicals: multi-year reshape + leverage to a turn.

Two brief global-growth theses: one China platform, one media leader.

Asian fiber broadband: capex fading, FCF inflection ahead.

Expert-market gas E&P: production ramp + big torque to gas prices.

Disclaimer: Nothing here constitutes professional and/or financial advice. You alone assume any risk with the use of any information contained herein. We may own positions in the securities listed. Please do your own due diligence.

To the investment managers who read this, you can send us your letters at elevatorpitches@substack.com or on Twitter (and Threads!) if you’d like to be included in a future issue.

Let’s get to it.

We’re kicking things off with a new idea from Greystone Capital Management, who recently initiated a position in Shift4 Payments (FOUR). Shares are down more than 40% over the past year, but Greystone argues the underlying business continues to execute, with expanding margins, strong organic growth, and disciplined capital allocation. Their pitch also serves as an excellent primer on the payments ecosystem, and why owning the full stack matters more than most investors realize.

“A complex system that works is invariably found to have evolved from a simple system that worked. The inverse proposition also appears to be true: a complex system designed from scratch never works and cannot be made to work.” -- John Gall, Systemantics

During the quarter, we initiated a position in Shift4 Payments, an integrated payments company with a long track record of operational execution and disciplined capital allocation. Founded in 1999 in a New Jersey basement, Shift4 has steadily built a leading position across hospitality, restaurant, and stadium end markets. While shares have declined more than 40% over the past year alongside much of the payments sector, the underlying business has continued to perform well, with solid organic growth, expanding gross margins, and the completion of its largest acquisition to date, Global Blue, during 2025.

Throughout its 26-year history, Shift4 has evolved substantially, pairing deep industry knowledge with a consistent ability to adapt as the payments landscape has changed. This combination of experience and ongoing iteration has created a durable competitive position, enabling the company to continue gaining share across restaurant, stadium, and resort verticals while increasingly embedding merchants into its end-to-end payments ecosystem. Despite this progress and a long runway for continued growth, the market is valuing Shift4 as a legacy, leveraged payments processor, rather than as a recurring, high-retention platform characterized by strong incremental margins, meaningful switching costs, and a differentiated operating culture.

Under conservative assumptions, Shift4 has the potential to grow revenue and free cash flow at a 20–25% rate over the coming years, a trajectory that should support a higher valuation as execution continues. With a founder-led management team focused on disciplined capital allocation, an active share repurchase program covering roughly 20% of shares outstanding, and a compelling starting valuation, FOUR offers an attractive long-term risk-adjusted return profile.

------------------------------

In Arthur Rankin’s 1969 Frosty the Snowman cartoon, there’s a scene where Professor Hinkle, the world’s worst magician, attempts what he thinks is a simple trick. He drops a few eggs into his hat, flips it over, and expects birds to fly out. Instead, the eggs spill and shatter on the floor. He looks down at the mess and mutters, “messy, messy, messy.” My kids love that scene.

But the joke is not simply that Professor Hinkle is a bad magician; it’s that he mistakes a deeply complex trick for a simple one. Turning eggs into birds requires mastering a long chain of hidden steps. Hinkle ignores that complexity, and reality asserts itself in the mess on the floor.

Payment businesses appear simple on the surface. Swipe a card, a transaction clears, the merchant gets paid. In reality, they are closer to Professor Hinkle’s trick, full of complexity and multiple failure points. This distinction, between problems that appear simple versus those that are simple only after doing the hard work of internalizing complexity, is directly related to our investment in Shift4, where the company has a decisive advantage as a company that has learned how to contain that complexity, so their customers don’t have to.

Shift4 is an integrated, end-to-end payments business. The company was founded by former CEO (now Executive Chairman) Jared Isaacman, remarkably at the age of 16, and has since grown into the leading provider of software and payment processing solutions to various end markets. The company powers billions of transactions for a diverse set of small business and enterprise customers and holds the #1 spot in hospitality, sports and entertainment, global luxury retail, and the #2 spot in restaurants. The ideal customer for Shift4 is characterized by a small business utilizing a variety of software and hardware tools to operate their business and accept payments.

In the payments value chain, Shift4 acts as a merchant-facing provider, essentially a one-stop combination of payment gateway, payments processor, and point-of-sale (POS) software. Shift4’s model consists of managing the software that merchants use to accept payments, while also managing the back-end payment acceptance (or rails) that process each transaction. FOUR’s value prop is made up of their ability to integrate the ‘full stack’ of software, hardware and payments in complex, card-present and not-present environments.

If you’ve ever visited a hotel with various purchase points across the property – front desk, spa, restaurants, gift shop – FOUR takes the different software required to accept payments at each purchase point, and integrates them into one single-source solution, making the customer’s life (in this case, the hotel) more efficient and lower cost. Instead of managing multiple pieces of hardware, multiple support systems, and multiple transactions reports, Shift4 integrates everything into one unified system. In other words, as discussed, FOUR absorbs the complexity of disparate systems and software and spits out a simplified solution for the customer.

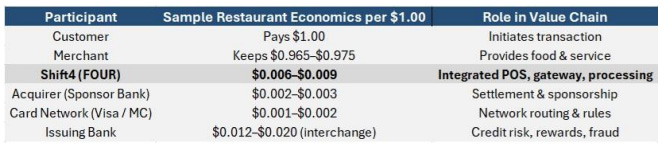

Shift4 is uniquely positioned relative to most payments companies because it owns the gateway layer, allowing it to sit structurally between the merchant and the acquirer. This control enables Shift4 to embed payments directly into mission-critical POS and commerce software, retain a larger share of transaction economics, and flex pricing without relying on third-party processors, rather than competing as a standalone, price-taker processor.

On a $1.00 card transaction in a typical restaurant, the economics flow as such:

Shift4’s one-stop-shop offering and vertical focus highlight the underlying strength of its business model. Historically, many payments and commerce software companies, including Toast (TOST), Block (XYZ), Lightspeed (LSPD), and NCR Voyix (VYX), have led with hardware and feature-rich POS systems, building sticky customer bases and recurring software revenue while treating payments as a secondary concern and outsourcing transaction processing to third-party providers. This approach reflects the long-held view that payment routing alone adds little value, as gateway-only models are commoditized, low-margin, and easily replaced. I don’t disagree. But by owning the economics of transaction capture and settlement, Shift4 can retain a spread and generate meaningful gross profit, rather than earning the residual economics associated with simple transaction routing.

This allows FOUR to scale with payment volume as opposed to customer count and meaningfully reduce churn. FOUR notes 1.0% churn among their top 50 customers and less than 3.0% total annual merchant churn. By integrating solutions and providing end-to-end payment capabilities, FOUR turns the commodity of payment processing into a sticky service offering, can earn a larger share of the economics per transaction, can tailor its platform to various industries (stadiums, restaurants, hotels) and can share a portion of the economics with customers in the form of reduced hardware and software fees.

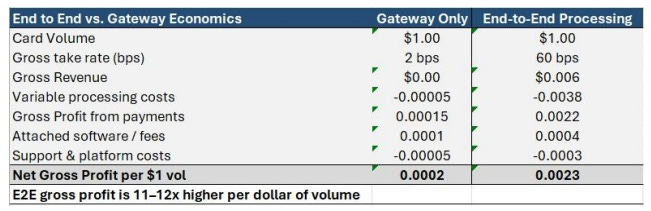

Given these dynamics, Shift4 is naturally focused on deepening its relationships with merchants, with the growth strategy centered on expanding end-to-end payment volume within each vertical while systematically converting gateway-only customers to full processing. The company is uniquely positioned to execute this given its 550 software integrations, lower price offerings, and scale. It’s scale that allows Shift4 to subsidize POS hardware and offer targeted financial incentives in exchange for exclusive payments relationships. Converting gateway customers to end-to-end processing is a core strategic lever and a powerful unlock for both revenue and margin expansion.

Using a restaurant example, the contrast between gateway-only transactions and full end-to-end processing illustrates the step-change in unit economics. For an identical dollar of volume, end-to-end processing generates meaningfully higher gross profit, underscoring why merchant conversion is central to Shift4’s strategy.

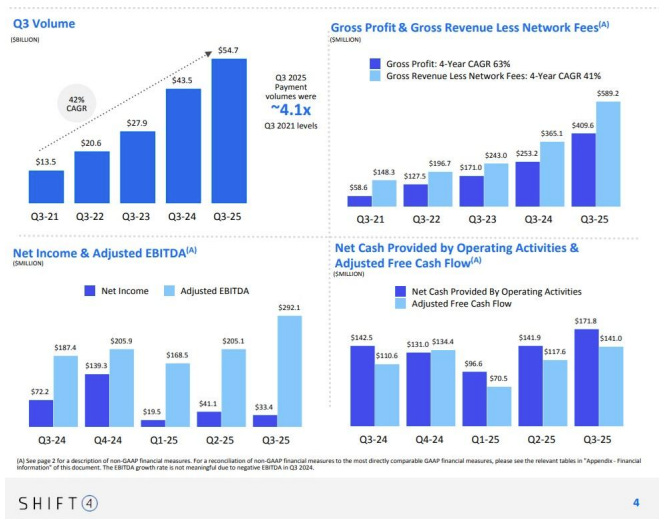

As a result, the economics of end-to-end conversion have translated directly into accelerated financial performance. Shift4’s payment volume has grown more than 4x since 2021, but net revenue and gross profit have expanded far faster as higher-margin end-to-end volume replaced lower-value gateway activity. Net revenue has reflected a CAGR of approximately 41% annually since 2021, while gross profit growth has exceeded 60%, driven by the superior unit economics of end-to-end processing.

Next, organic growth is complemented by disciplined M&A. When entering new verticals, management evaluates whether to build, partner, or acquire, and has consistently favored acquiring mission-critical software with an embedded customer base and under-monetized payment flows. This approach allows Shift4 to step directly into established workflows, convert existing customers to end-to-end payments, and do so at an attractive average cost of acquisition.

A clear example is Shift4’s acquisition of VenueNext to enter the stadium vertical. VenueNext provided mobile in-seat and in-venue ordering across large sports and entertainment venues but had not fully monetized payments. By integrating VenueNext into Shift4’s end-to-end payments platform, the company was able to turn a software engagement layer into a high-margin payments annuity, rapidly scaling penetration across a complex, high-volume vertical.

Despite pursuing an M&A-heavy strategy, the consistency of execution and the attractive return profile of recent deals stand out in an industry where M&A often destroys value. Shift4’s historical results suggest a repeatable playbook rather than isolated successes, which I discuss in more detail below.

Shift4’s M&A strategy also highlights a fundamental difference in how the company scales relative to most peers. While many software and payments businesses rely heavily on sales and marketing to acquire merchants and attempt to monetize payments later, Shift4 has instead used acquisitions and hardware deployment as its primary customer acquisition tools. This approach allows the company to enter merchant workflows directly, embed payments at the point of operation, and convert existing transaction volume into high-margin, recurring payment revenue.

By contrast, competitors such as Toast and Lightspeed must spend aggressively on customer acquisition and recover those costs through a combination of software subscriptions and shared payment economics. The Shift4 model not only materially lowers upfront costs for the merchant but accelerates payback periods and increases lifetime value. Over time, this shifts economics away from transactional customer acquisition and toward a recurring payments annuity. Importantly, Shift4’s is acquiring already established businesses, lowering integration risk and allowing them to monetize the part of the value chain Shift4 controls best, payments.

As a result, while Toast, Lightspeed, and Shift4 may appear to offer similar functionality to merchants at comparable all-in costs, the underlying economics diverge meaningfully. Shift4’s ownership of the full stack allows it to retain a larger share of the payments spread, translating incremental volume into disproportionately higher free cash flow. Peers have far less pricing flexibility and lower incremental margins at scale.

While software often attracts the most attention, Shift4 is not competing to deliver the most elegant POS interface or the richest feature set. Instead, the company is focused on owning the most valuable control points in complex verticals. While Shift4 is not alone in recognizing the value of owning the full payments stack, competitors attempting to move in the same direction are discovering how difficult it is to replicate what Shift4 has built organically over decades.

External validation for the intractability of payments and the value of owning the full stack can be found in the strategy of NCR Voyix. NCR’s core business historically centered on POS and software, but it repeatedly ran up against the limits of a fragmented payments model, relying on partnerships with processors like Worldpay to deliver integrated payments to its customers. That dynamic forced NCR to share economics and coordination complexity with third parties instead of owning the transaction lifecycle. As NCR’s leadership noted, they selected Worldpay specifically because of the complexity of their customer base, implicitly acknowledging that embedded payments cannot be abstracted away through loose integrations or partnerships alone. This validates a core tenet of the Four thesis: the economics of payments accrue most sustainably when the stack is owned end-to-end, not parceled out through external processors.

------------------------------

Importantly, the decision to build end-to-end payments capabilities was not an accident, but the result of decades of operating experience and iteration. A useful distinction in investing is between tractable and intractable problems. Tractable problems can be decomposed, standardized, and solved with sufficient capital or effort. Intractable problems, by contrast, are path-dependent and resistant to linear solutions, requiring cumulative learning over time rather than optimization in a single step. Integrating software, hardware, and payments across complex merchant environments falls firmly into the latter category.

Enduring businesses often emerge by starting with a narrow problem and gradually expanding their capabilities through repeated trial, error, and adaptation. The resulting advantage is not complexity for its own sake, but the learning embedded in the system itself. A competitor beginning from a standing start cannot simply replicate the end state, regardless of resources, because the knowledge required to operate the system effectively is accumulated only through experience.

By the time FOUR went public in 2020, the company had spent nearly two decades working through multiple verticals, end markets, and product iterations. Along the way, it developed deep integration capabilities across hundreds of software systems, acquired control of the payment gateway, and converted under-monetized platforms into full end-to-end payment solutions. That process produced a body of institutional knowledge that cannot be reverse engineered from the outside and makes the business meaningfully harder to dislodge than surface-level metrics suggest.

This distinction between tractable and intractable problems explains much of what the market is missing here.

------------------------------

At today’s price, Shift4 trades at a mid-single-digit multiple of EBITDA and roughly 10x my estimate of 2026 earnings. While Shift4’s revenue is more cyclical than that of pure software businesses, the current valuation implies a level of fragility that understates the durability of the underlying business. Despite volume sensitivity, Shift4 exhibits many software-like characteristics, including embedded workflows, low churn, meaningful switching costs, pricing control, and capital allocation flexibility that allows management to redirect effort toward merchant conversion, M&A, and share repurchases during periods of weaker demand.

In contrast, the market appears to reward companies such as Toast primarily for the contractual nature of their software revenue, while discounting Shift4 for its exposure to transaction volumes, even though Shift4’s economics increasingly converge with software-like models at scale. The result is a wide valuation gap, with Toast trading at approximately 24x EBITDA and 28x earnings versus Shift4 at roughly 7x EBITDA and 10x earnings, that I believe overstates the difference in long-term durability and understates Shift4’s ability to show strength through the cycle. A similar disparity exists relative to Lightspeed, which trades at materially higher multiples despite lower profitability and less control over payment economics.

Using conservative estimates, including no incremental M&A, modest Global Blue conversion, and a dip in continued installed base monetization, earnings power should grow to around $8/share by 2028. This also assumes management fails to execute the $1.0B share repurchase program in place which would retire 20% of shares outstanding. Using the same assumptions but factoring in just half the buyback authorization would increase EPS to $9.0/share, or 7.0x earnings. I’m not arguing that FOUR deserves a SaaS multiple, but at just 14x earnings, half of Toast’s multiple, shares would be worth $112/share versus $63 today, driving a 21% 3-year IRR.

I view this outlook as overly conservative due to management’s enthusiasm for the buyback, incremental EBITDA kicking in from 2024 acquisitions, and the remaining top of the funnel opportunity to convert merchants to FOUR’s end to end payment processing. What’s more likely is that FOUR will continue to convert merchants at a strong clip, successfully integrate Global Blue while converting a decent portion of the merchant base, de-lever modestly and repurchase stock. If successful just doing what they’ve done since their IPO, my estimate of adjusted earnings/free cash flow (adjusted for hardware acquisitions and stock-based compensation) could reach $10-11 share within the next few years, implying a $140-155 share price. This would largely track management’s target of a $1.0 billion free cash flow run rate within the next two fiscal years without giving much credit for incremental M&A, which could add to free cash flow per share over time.

As mentioned above, management has demonstrated the ability to reinvest large amounts of capital at high unlevered returns over multiple years. Since 2019, the company has deployed roughly $2.7 billion of growth-related capital across customer acquisition, product investment, and M&A, generating approximately $515 million of incremental EBITDA, even after burdening results for stock-based compensation and recurring integration costs. This equates to an unlevered return on invested capital of roughly 19.0%, before accounting for 2024 acquisition synergies and any contribution from 2025 onward.

Most importantly, the market is valuing Shift4 as if success depends on continuous merchant acquisition and M&A. Growth would persist even without new acquisitions. If Shift4 were to cease M&A entirely and simply continue converting its installed base, or what management calls ‘sitting on their hands’, the business would still grow organically in the mid-to-high teens, while free cash flow would inflect sharply higher as growth capex moderates. As a reminder, a meaningful portion of future value creation comes from monetizing an already-installed gateway base, as moving a merchant from gateway-only to end-to-end processing increases gross profit per merchant significantly, without requiring incremental customer acquisition. That is quite attractive and points to the high margin annuity that is end-to-end payments.

While Shift4 is not immune to cyclical pressures given its end markets, ongoing merchant conversions and increasing payment adoption make the business more durable than the market currently recognizes.

From a management perspective, we are invested alongside a true owner-operator with meaningful alignment. Founder and CEO Jared Isaacman retains roughly a 30% economic interest in the business and has guided Shift4 through decades of iteration to what I believe is its strongest competitive position to date, reinforced by multiple open-market share purchases during 2024 and 2025, including a $16.0 million purchase in August of last year. Importantly, prior governance concerns have been addressed through the elimination of multiple share classes and a legacy tax receivable liability, while management’s demonstrated willingness to repurchase undervalued shares and pursue opportunistic M&A, particularly in weaker economic environments, adds further confidence, supported by management’s experience navigating and growing through the Financial Crisis.

Most importantly, since Shift4’s IPO, management has largely exceeded all expectations and has a history of under-promising and over-delivering. Since their IPO in 2020, FOUR has compounded shareholder capital at 20.5% per year, outpacing the S&P500 by 400bps per year. While a successful return is not dependent on this outcome, it’s possible Jared is positioning the company for a sale at some point during the next few years. FOUR has received offers in the past, but at a share price not high enough to tempt management, and before Jared was named NASA’s 15th Administrator.

While the outcome will ultimately depend on execution, I am comfortable owning FOUR alongside a strong, founder-led management team. As the company continues to grow organically, integrates Global Blue, expands payment penetration across its existing customer base, repurchases shares, and demonstrates resilience through the cycle, I believe the underlying quality and durability of the business should become increasingly evident to the market and eventually support a higher valuation.

Five more stock pitches below, available to paid subscribers.

If you find value in seeing how professional investors frame new ideas, upgrade to keep reading and get the full archive.

Need a nudge? Many subscribers work in asset management, research, or corporate finance and expense it as a research tool. Here’s a quick script you can use.

Hi [Manager’s Name],

I’d like to expense a subscription to Elevator Pitches, a newsletter that curates stock ideas from professional investor letters, often highlighting overlooked opportunities and special situations.

With a paid subscription, I’d receive full access to every stock write-up they publish each week, which would support my ongoing market research and idea generation.

The cost is $90 for the full year. Given the depth and frequency of the analysis, I think it’s a cost-effective addition to my research toolkit.

Please let me know if this works.

Best,

[Your Name]